Is there even such as thing as the “Ides

of October”? Probably not. But perhaps there should be. At least when it comes to gold stocks.

First a great big caveat: Seasonality

overall has not been as useful in 2020 as in previous years. So, there is no reason gold stocks cannot register

a meaningful gain in October of this year.

But investing and trading is as much a game of odds as anything

else. And the odds, generally speaking,

are unfavorable for gold stocks in the month of October.

Gold Stocks in October

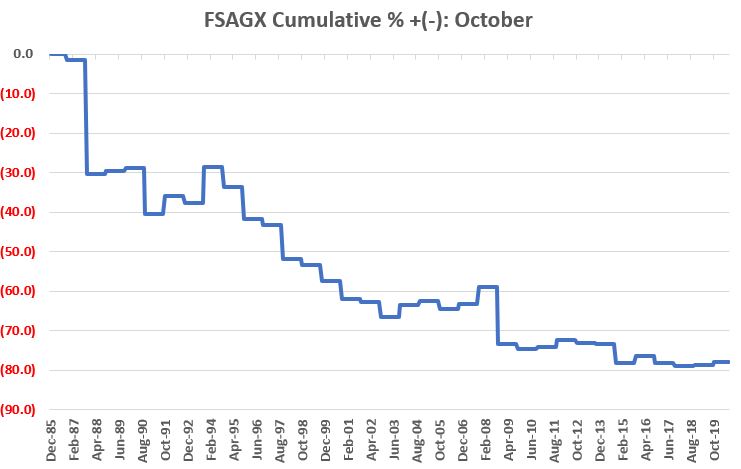

We will use Fidelity Select Gold (FSAGX) as our proxy as there is monthly data going back to 1986. Figure 1 displays the cumulative return an investor would have achieved by buying and holding FSAGX every year since 1986 ONLY during the month of October. For the record, the result to date is a loss of -78%.

Figure 1 – Cumulative %+(-) for FSAGX

only during month of October; 198-2019

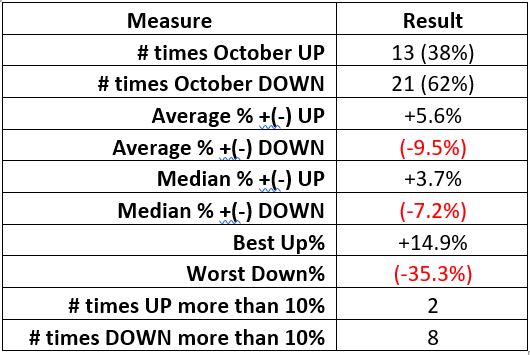

Things to note:

Figure 2 – Relevant Facts and Figures

Figure 3 displays year-by-year total

return results for FSAGX during the month of October.

Year

% +(-)

Oct-86

(1.4)

Oct-87

(29.2)

Oct-88

1.0

Oct-89

1.0

Oct-90

(16.4)

Oct-91

7.7

Oct-92

(3.0)

Oct-93

14.9

Oct-94

(7.2)

Oct-95

(12.1)

Oct-96

(2.7)

Oct-97

(15.3)

Oct-98

(3.0)

Oct-99

(8.4)

Oct-00

(11.0)

Oct-01

(1.9)

Oct-02

(10.5)

Oct-03

9.6

Oct-04

2.6

Oct-05

(5.7)

Oct-06

3.7

Oct-07

12.1

Oct-08

(35.3)

Oct-09

(4.4)

Oct-10

1.9

Oct-11

6.7

Oct-12

(3.1)

Oct-13

(0.7)

Oct-14

(17.9)

Oct-15

7.6

Oct-16

(7.3)

Oct-17

(3.4)

Oct-18

1.2

Oct-19

2.9

Figure 3 – FSAGX in October Year-by-Year; 1986-2019

Summary

In the current market environment, there

is no reason that gold stocks cannot rally substantially to the upside in the

month ahead.

Gold stocks (using FSAGX as a proxy)

have showed a gain in each of the last 2 Octobers and have done so 38% of the

time. So, the proper way to look at the

data above IS NOT to say “gold stocks are doomed to fall in the month ahead.”

The proper response is to ask

yourself the question, “is this where I want to allocate money right now?”

See also Jay Kaeppel Interview in July 2020 issue of Technical Analysis of Stocks and Commodities magazine

Disclaimer: The information, opinions and ideas expressed herein are for

informational and educational purposes only and are based on research conducted

and presented solely by the author. The

information presented represents the views of the author only and does not constitute

a complete description of any investment service. In addition, nothing presented herein should

be construed as investment advice, as an advertisement or offering of

investment advisory services, or as an offer to sell or a solicitation to buy

any security. The data presented herein

were obtained from various third-party sources.

While the data is believed to be reliable, no representation is made as

to, and no responsibility, warranty or liability is accepted for the accuracy

or completeness of such information.

International investments are subject to additional risks such as

currency fluctuations, political instability and the potential for illiquid

markets. Past performance is no

guarantee of future results. There is

risk of loss in all trading. Back tested

performance does not represent actual performance and should not be interpreted

as an indication of such performance.

Also, back tested performance results have certain inherent limitations

and differs from actual performance because it is achieved with the benefit of

hindsight.

Now back in the day I might have been

embarrassed to write an ostensibly bullish piece titled “What’s Up with

[Whatever]?” only to have [Whatever] completely fall apart immediately thereafter. But here are the important parts:

First:

*There is a critical distinction

between identifying a “potentially bullish” situation and actually risking money

Second:

The trading process – at least for me

– involves:

*Identifying a potential bullish or

bearish setup

*Identifying a catalyst or trigger

*Making a trade

The original article covered only

Step #1 of the trading process – identifying a setup. The closing sentences from the 9/14 piece stated,

“But if one was considering making a bullish play in silver, it may be getting

close to time to do so. My favorite play

would be something using options with a relatively low cost and low dollar

risk. Stay tuned…”. In other words, no action is warranted at the

moment, let’s see what transpires. Well

now we know:

*Spectacularly, ridiculously, (almost)

embarrassingly wrong in terms of direction and timing.

*But the setup was there, so as a trader

the proper response is to prepare to make a trade

*At the time (although I did not

mention this specifically in the original article) I was looking for a breakout

of consolidation to the upside as a catalyst to make a bullish trade

And then BLAM – the bottom drops

out. As a trader I put this down as “No

Harm, No Foul”.

So, is that “The End”? Not for me.

As you can see in Figures 2 and 3, the daily and weekly Elliott Wave

counts from ProfitSource by HUBB are both still potentially bullish, believe it

or not.

*The longer silver stays down the

more likely these wave counts will ultimately get “redrawn” (which is why I am

not a fully committed “Elliott Head” but use it only when the daily and weekly

counts agree)

*As you can see in Figure 3, silver

has now fallen to a level which could complete Wave 3 down and (possibly) set

the stage for a Wave 4 up

*In Figure 2 the bullish daily Wave 4

count remains intact (although as I just mentioned “for how long?” does remain

an issue)

As you can see in Figure 4, the

recent plunge in silver has driven bullish sentiment for the silver ETF ticker

SLV to an extremely low level (only 1.2% of SLV traders surveyed are presently

bullish!).

Disclaimer: The information, opinions and ideas expressed herein are for

informational and educational purposes only and are based on research conducted

and presented solely by the author. The

information presented represents the views of the author only and does not

constitute a complete description of any investment service. In addition, nothing presented herein should

be construed as investment advice, as an advertisement or offering of investment

advisory services, or as an offer to sell or a solicitation to buy any

security. The data presented herein were

obtained from various third-party sources.

While the data is believed to be reliable, no representation is made as

to, and no responsibility, warranty or liability is accepted for the accuracy

or completeness of such information.

International investments are subject to additional risks such as

currency fluctuations, political instability and the potential for illiquid

markets. Past performance is no

guarantee of future results. There is

risk of loss in all trading. Back tested

performance does not represent actual performance and should not be interpreted

as an indication of such performance.

Also, back tested performance results have certain inherent limitations

and differs from actual performance because it is achieved with the benefit of

hindsight.

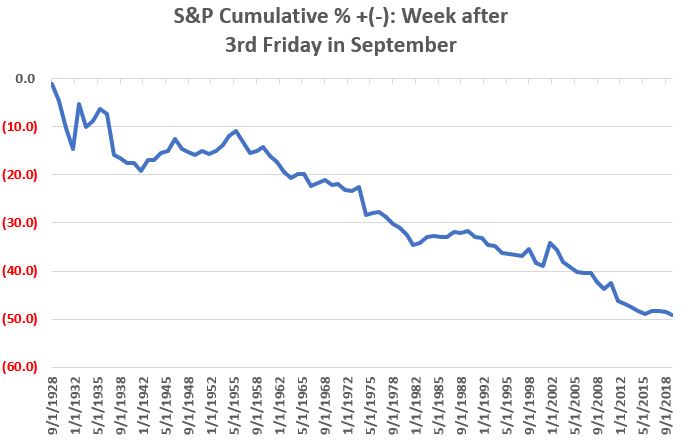

I have written in the past about the “dangers” of September (see here and here) and a lot of investors are aware that it has historically been the worst month of the year for the stock market overall. But the truth is things can vary a lot from year to year – except for this week. This week – defined as the week after the 3rd Friday in September – has been pretty awful pretty consistently for a pretty long time. As you may gather, no, it has not been pretty.

Two of my favorite analysts – Wayne Whaley of Witter & Lester and Rob Hanna of www.QuantifiableEdges.com both made light of this recently. The bottom line:

*The week after the 3rd Friday

in September has seen the S&P 500 decline in 24 of the last 30 years.

Being the numbers geek that I am I

went back to the start of my own database in 1928. I found that in the prior 31 years this week

was up 14 times and down 17 times.

While at first blush this “doesn’t

sound as bad”, the reality is that given the magnitude of the overall market

advance since 1928, that this particular week is so consistently NOT bullish is

downright dismal. Especially when we

consider the magnitude of the ups versus the downs and the overall long-term

trend.

The Numbers

Since 1928, the week after the 3rd

Friday in September has seen the S&P 500 Index:

*Advance 33 times

*Decline 54 times

*Unchanged once

*Average gain = +1.64%

*Average loss = (-2.04%)

Figure 1 displays the cumulative % +(-) achieved by the S&P 500 Index since 1928 during the week after the 3rd Friday in September.

Figure 1 – Cumulative % return for

S&P 500 Index ONLY during week after 3rd Friday in September

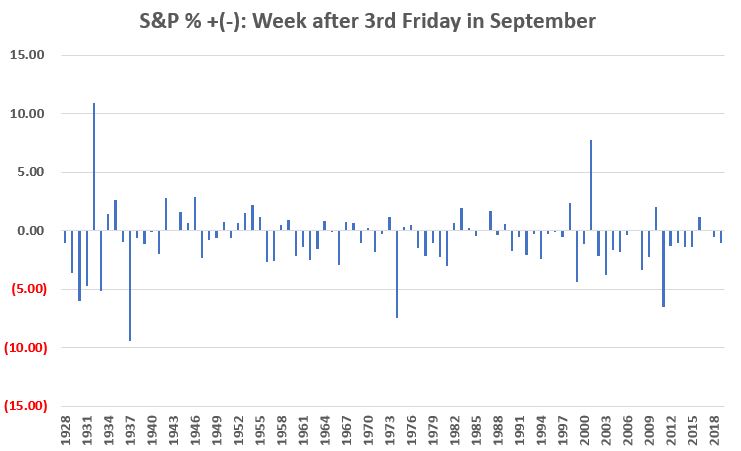

Figure 2 displays the year-by-year

results.

Figure 2 – Week after 3rd

Friday in September Year-by-Year % +(-)

September “Hell Week” for 2020 is off

to a pretty dismal start. Will things improver

anytime soon? It beats me. But I am of the mind that during September

and October “anything can happen” so investors should be prepared. I am also of the mind that starting in November

the bullish trend will re-assert itself.

Here’s hoping.

On a slightly separate note – even a down September is not totally without value thanks to the “September Barometer” (see here and here).

See also Jay Kaeppel Interview in July 2020 issue of Technical Analysis of Stocks and Commodities magazine

Disclaimer: The information, opinions and ideas expressed herein are for

informational and educational purposes only and are based on research conducted

and presented solely by the author. The

information presented represents the views of the author only and does not constitute

a complete description of any investment service. In addition, nothing presented herein should

be construed as investment advice, as an advertisement or offering of

investment advisory services, or as an offer to sell or a solicitation to buy

any security. The data presented herein

were obtained from various third-party sources.

While the data is believed to be reliable, no representation is made as

to, and no responsibility, warranty or liability is accepted for the accuracy

or completeness of such information.

International investments are subject to additional risks such as

currency fluctuations, political instability and the potential for illiquid

markets. Past performance is no

guarantee of future results. There is

risk of loss in all trading. Back tested

performance does not represent actual performance and should not be interpreted

as an indication of such performance.

Also, back tested performance results have certain inherent limitations

and differs from actual performance because it is achieved with the benefit of

hindsight.

As people age, very often investing

becomes more about “keeping what you have” and less about “making more.” Oh sure, more is still always better. But the bottom line is there comes a point

when Will Rogers old adage below becomes relevant.

“I’m less interested in the return on

my money as I am the return of my money” Will Rogers

To this end, in this piece we will

focus on one possible approach to “low risk investing” (which of course makes

the assumption that there is such a thing).

The Components

Ticker VTIP ( Vanguard Short-Term Inflation-Protected Securities Index Fund ETF)

VTIP holds short-term TIPs

bonds. TIPs are treasury bonds that are indexed

to inflation. A newly issued TIPs bond has

a principal value of $1,000 and pays a stated percentage of interest on that

principal. Moving forward, if the

Consumer Price Index rises, the principal amount of the bond is adjusted

upward, and interest is paid as a percentage of the higher principal

amount. If inflation were to soar, a

TIPs bond could end up paying a lot of interest, hence the reason they are considered

a hedge against inflation.

On the other side of the coin, if we

have deflation and the CPI declines, then the principal amount for a TIPs bond

gets adjusted lower and interest is paid on this lower amount. HOWEVER, keep in mind that each TIPs security

is repaid the full $1,000 original face value at maturity and the effective

maturity of VTIP is roughly 2.9 years.

So even if the principal amount gets adjusted lower temporarily

(resulting in lower interest payments for the time being), at maturity the full

$1,000 is repaid. This makes deflation

less of a concern for a short-term TIPs holder than for a long-term TIPs

holder.

Speaking of long-term versus

short-term bonds, long-term TIPs can get hurt by rising interest rates. Short-term bonds are less impacted by rising

rates as they mature much sooner.

Ticker SHY ( iShares 1-3 Year Treasury Bond ETF)

Ticker SHY holds treasury securities

that mature in 1 to 3 years. The reality

is that with interest rates presently so low the only way to make money on

short-term bonds is if rates go even lower, or possibly even into negative

territory. However, this portion of the portfolio is a play on safety and low

volatility. If interest rates were to rise, a) short-term bonds would be much

less sensitive in terms of any price decline than longer-term bonds, and, b) if

interest rates were to embark on a sustained increase, short-term bonds would

be able to roll over into higher yielding securities sooner and on a more

frequent basis than longer-term bonds.

I am always a bit leery of securities

that seem “gimmicky”. SWAN may be

thought of as such by some investors.

But in the context of our “lower risk approach” it can be a portfolio

enhancer. Ticker SWAN holds roughly 90%

of its portfolio in treasury securities (with a duration roughly equivalent to

a 10-year treasury). This portion of the

portfolio has no credit risk and moderate interest rate risk (i.e., the value

of the bond holdings may increase if rates decline or decrease if rates rise).

The other 10% holds exposure to the

S&P 500 Index in the form of LEAPs call options. This gives the portfolio the potential to

gain during an advance in stocks. While this portion of the portfolio will

decline during a stock market decline, the bond holdings can serve as a

“buffer”, as treasury securities often rally during stock market declines as

investors flee to investments perceived to be “safe”.

Putting the Portfolio Together

First a few caveats/footnotes:

*For the record, I am not actually

advocating that anyone run out and put money into this idea. At the moment, it is just that – an idea,

food for thought. This portfolio will

rarely make a lot of money, AND it is possible that a given scenario (possibly

an excessively large “spike” in interest rates, perhaps) could create a larger

loss than what was experienced in back testing.

*For testing purposes, I used ETF

total return data wherever possible.

Prior to that I used either index data or a comparable ETF in order to

generate a longer back test. So DO NOT

mistake the results below as “real time” results. The results depicted are strictly a

hypothetical representation of hat real world results might have

resembled. And as always, past performance

is no guarantee of future results.

*For VTIP, I used Adjusted Close data

from Yahoo (which is believed to account for price changes and dividend income)

for ticker TIP (which has a longer duration that ticker VTIP) from 12/6/2005

through 10/16/2012, when VTIP started trading. From that date forward VTIP

Adjusted Close data from Yahoo is used.

*For SHY, I used Adjusted Close data from

Yahoo (which is believed to account for price changes and dividend income) for

ticker SHY from 12/6/2005 to the present.

*For SWAN, I used total return daily

data for the Index that ticker SWAN is designed to track from 12/6/2005 through

11/6/2018, when SWAN started trading. From that date forward SWAN Adjusted

Close data from Yahoo is used.

Are we having fun yet?

The Portfolio

For our purposes we will keep it

simple – 1/3 in each ETF with a rebalance at the beginning of every year.

VTIP = 33%

SHY = 33%

SWAN = 33%

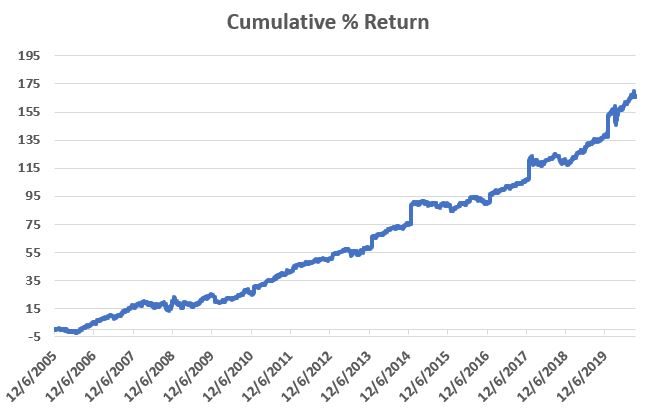

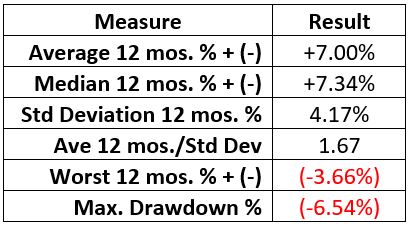

The Results

Figure 1 displays hypothetical

cumulative return for the portfolio from December 6, 2005 through 9/16/2020.

*The standard deviation of 12-month

returns is 4.17% (i.e., low)

*The maximum % drawdown was -6.54%

(i.e., low)

Figure 3 displays the annual % gain on a calendar year basis.

Figure 3 – Annual hypothetical

results

*The key thing to note is that – so

far – there have been no down years.

Summary

Once more for the record, I am not “recommending”

this portfolio. I am merely pointing out

that for a person who was seeking decent returns with relatively low risk and

low volatility, hypothetically speaking this one hasn’t been half bad.

Still, one has to consider potential

risks before committing real money to anything.

I can envision at least one scenario – the stock market tanks BECAUSE interest

rates are spiking BUT inflation remains relatively low – where this portfolio

could have some more serious trouble.

There may be others.

All in all, though, not the worst

idea as food for thought for investors looking for a low risk approach.

See also Jay Kaeppel Interviewin

July 2020 issue of Technical Analysis of Stocks and Commodities magazine

Disclaimer: The information, opinions and ideas expressed herein are for

informational and educational purposes only and are based on research conducted

and presented solely by the author. The

information presented represents the views of the author only and does not constitute

a complete description of any investment service. In addition, nothing presented herein should

be construed as investment advice, as an advertisement or offering of

investment advisory services, or as an offer to sell or a solicitation to buy

any security. The data presented herein

were obtained from various third-party sources.

While the data is believed to be reliable, no representation is made as

to, and no responsibility, warranty or liability is accepted for the accuracy

or completeness of such information.

International investments are subject to additional risks such as

currency fluctuations, political instability and the potential for illiquid

markets. Past performance is no

guarantee of future results. There is

risk of loss in all trading. Back tested

performance does not represent actual performance and should not be interpreted

as an indication of such performance.

Also, back tested performance results have certain inherent limitations

and differs from actual performance because it is achieved with the benefit of

hindsight.

Much has been written about the vast disparity in the performance of large-cap stocks versus small-cap stocks and of growth stocks versus value stocks. And an equal amount of speculation keeps raising the question of how long the current trends can last and when things will reverse.

What to make of all this?

Let’s try to make it easy.

The Comparison

For our purposes we will use monthly

total return data starting in January 1979 for:

*Large cap growth (using the Russell

1000 Growth Index)

*Small cap value (using the Russell

2000 Value Index)

Clearly these two indexes represent a

vastly different subset of stocks.

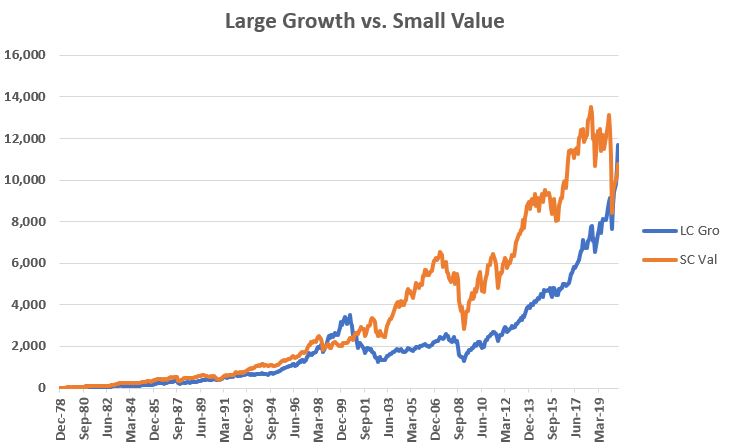

Figure 1 displays the cumulative

total return for both indexes starting in 1979.

Figure 1 – Large cap growth (blue)

vs. Small cap value (orange); cumulative total return starting in 1979

Many investors would be surprised to learn that small-cap value had been outperforming by a fairly sizable margin not that long ago. Only recently did large cap growth once again “take the lead.”

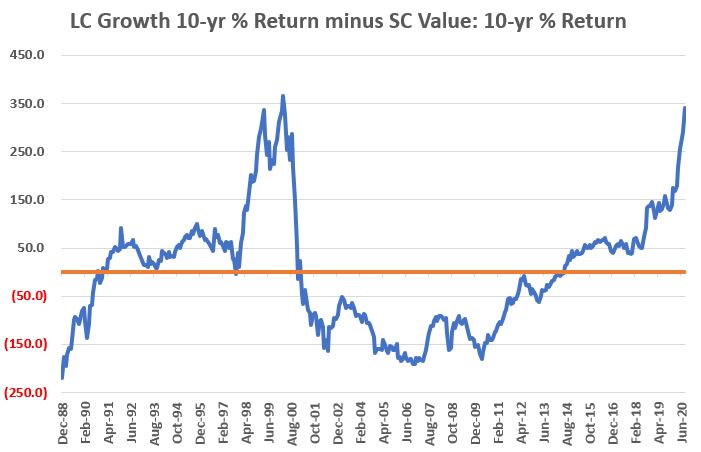

To get a better sense of the “back and forth” nature of this relationship, Figure 2 displays the 10-year cumulative return for large cap growth minus the 10-year cumulative return for small cap value starting in 1989.

Figure 2 – Cumulative 10-yr % return

for Large cap growth minus Cumulative 10-yr % return for Small cap value

To read Figure 2 – if the blue line

is above 0 it means large cap growth has outperformed small cap value over the

past 10 years, and vice versa. In a

perfect world this chart would eliminate all discussion of any “permanent edge”

for one index over the other. The lesson

SHOULD be obvious:

*Large cap growth leads for a number

of years, often by a wide margin

*Then small cap value leads for a

number of years – again, often by a wide margin

Clearly large cap growth has been

better of late and that trend still is in force. Figure 2 does remind us however, that this

trend WILL NOT last forever and that investors who pile into large cap growth

now need to pay close attention to the location of the nearest exit.

How to Use This Relationship

One approach is to use a 13-month

exponential moving average of the line in Figure 2 and note whether the line in

Figure 2 is above or below that 13-month average. These two lines appear in Figure 3.

Figure 3 – LC growth 10 yr. minus SC

value 10 year (blue) versus 13-month EMA (orange)

In Figure 3:

*If the blue line is above the orange line then the trend favors large cap growth.

*If the blue line is below the orange line then the trend favors small cap value.

So, let’s test the following

strategy:

NOTE: Total monthly return data is reported sometime early in the next month. So, because of this I use a 1-month lag in signals. Specifically, if I get total return data for January in early February and the results through the end of January signal a “switch” (i.e., if the 10-yr return for LC Growth minus the 10-yr return for SC Value crosses above or below the 13-month exponential moving average) then the actual switch will take place at the end of February

*If the blue line in Figure 3 moves

above the orange line in Figure 3 we will switch 100% into large cap growth

stocks (Russell 1000 Growth Index)

*If the blue line in Figure 3 moves below

the orange line in Figure 3 we will switch 100% into small cap value stocks

(Russell 2000 Value Index)

For comparison sake we will also compare

the results of this switching approach to simply buying and holding the Russell

1000 Growth Index and/or the Russell 2000 Value Index.

The % return for each appears in

Figure 4.

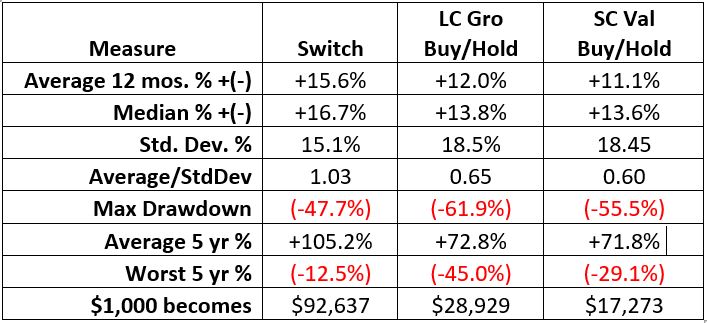

Figure 4 – Cumulative % return for “Switching”

versus simply buying and holding the indexes

Figure 5 displays some of the comparative

results.

Figure 5 – Switching versus Buying and Holding (1989-2020)

Summary

Switching between large cap growth and small cap value is by no means a perfect strategy (note the -47.7% drawdown for the switching strategy). But the real point is that this test clearly demonstrates that “falling in love” with one index over the other (as many have done in favor of large cap growth in recent years) is long-term a mistake.

A useful business adage is “Adapt or

Die.” Turns out it is pretty handy for

stock investors too…

See also Jay Kaeppel Interviewin

July 2020 issue of Technical Analysis of Stocks and Commodities magazine

Disclaimer: The information, opinions and ideas expressed herein are for

informational and educational purposes only and are based on research conducted

and presented solely by the author. The

information presented represents the views of the author only and does not

constitute a complete description of any investment service. In addition, nothing presented herein should

be construed as investment advice, as an advertisement or offering of investment

advisory services, or as an offer to sell or a solicitation to buy any

security. The data presented herein were

obtained from various third-party sources.

While the data is believed to be reliable, no representation is made as

to, and no responsibility, warranty or liability is accepted for the accuracy

or completeness of such information.

International investments are subject to additional risks such as

currency fluctuations, political instability and the potential for illiquid

markets. Past performance is no

guarantee of future results. There is

risk of loss in all trading. Back tested

performance does not represent actual performance and should not be interpreted

as an indication of such performance.

Also, back tested performance results have certain inherent limitations

and differs from actual performance because it is achieved with the benefit of

hindsight.

It has been nearly impossible lately to view the financial news in the 2020 and to not see some headline or story about “the coming explosion in Silver!!!!” (I left off a number of exclamation points in order to save space). While I do hold some bullish positions in metals it is more of a “trend-following thing” than an act of buying into the whole “MASSIVE RALLY AHEAD”.

Still, a quick recent look at all

things silver suggests that if “something big” is going to happen, a good chunk

of it might occur between now and the end of 2020. That’s not so much a “prediction” as it a “possibility

to be aware of.”

To wit:

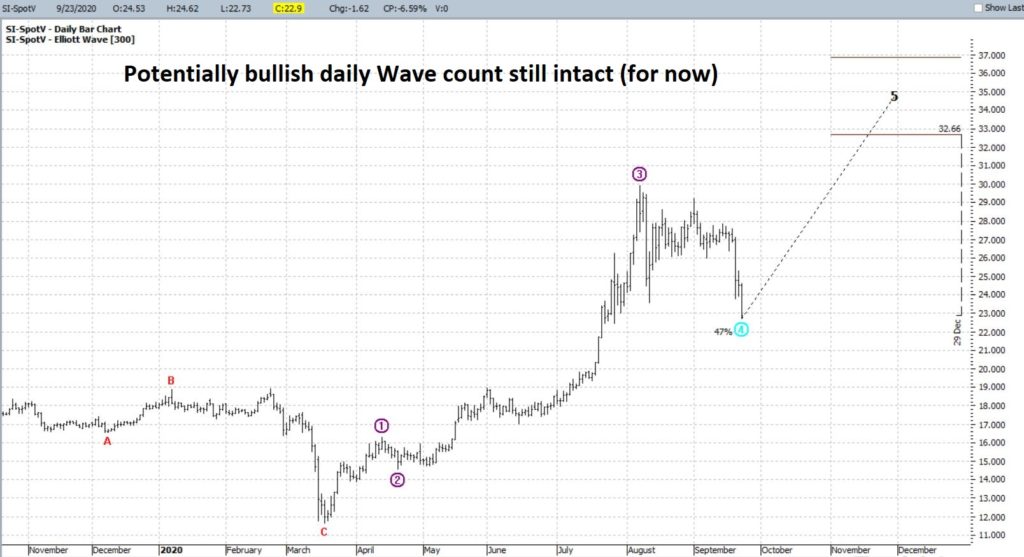

Figure 1 displays ticker SLV with a

daily Elliott Wave count calculated using the objective EW algorithm built into

ProfitSource by HUBB. As you can see,

the current projection is for rally to at least 29.87 by roughly the end of the

year.

Figure 2 displays ticker SLV with a weekly Elliott Wave count calculated using the objective EW algorithm built into ProfitSource by HUBB. As you can see, it is making a similar projection to the daily one, i.e., projecting a possible move toward $30 a share – in this case in late 2020 or early 2021.

*I am not a true “Elliott Head”, but

I do tend to pay attention when both the daily and weekly counts (using

ProfitSource) line up as bullish or bearish

*Elliott Wave counts from ProfitSource are like a lot of other things in the market – sometimes they pan out, sometimes they don’t. There is no “magic” involved. But the fact that they are generated “objectively” (as opposed to say Me picking what I subjectively “think look like wave counts”) gives me a bit more confidence.

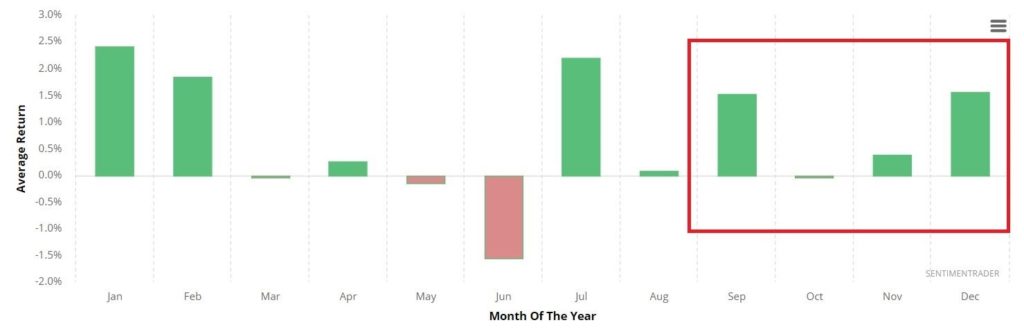

Figure 3 from www.Sentimentrader.com displays the monthly annual seasonal trend for silver futures. As you can see, the months ahead look fairly favorable. For the record, seasonality on the whole has seen a lot of things “out of whack” in 2020, so there is every chance this won’t pan out either. But for the moment I put it down as another factor in the “favorable” column.

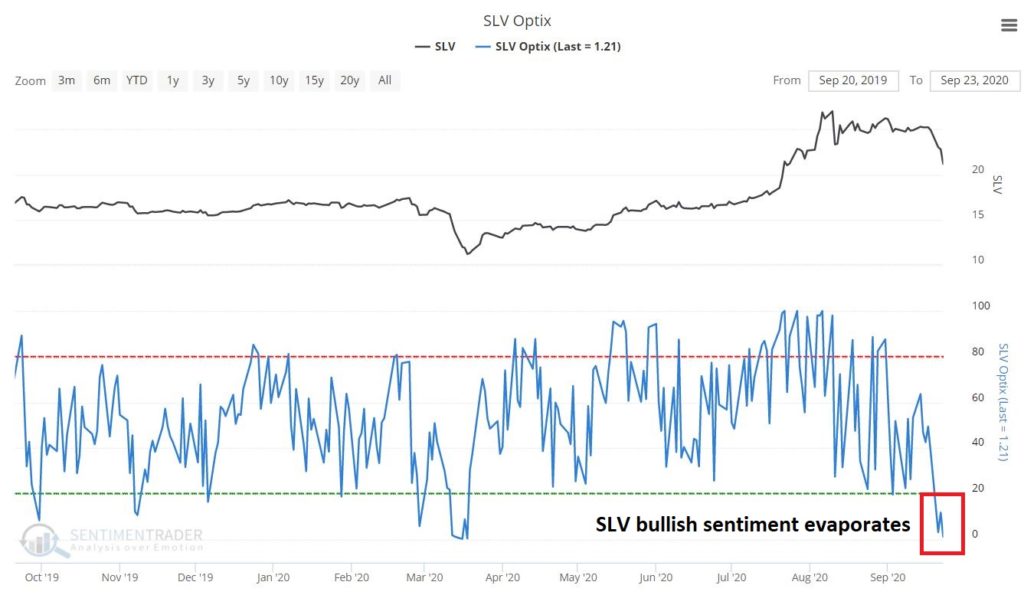

Figure 4 – also from www.Sentimentrader.com – displays the trader sentiment for ticker SLV. For the record, this one is presently technically (in my mind) “kinda neutral”. In other words, sentiment is neither excessively low nor excessively high.

Given that all “hubbub” surrounding

silver has been mostly bullish, I am actually counting it as a slight positive

that sentiment is presently not “off the charts” bullish. Looking at it this way may be seen as a bit

of a stretch to some, but it makes sense in my market-addled mind.

So, will SLV actually “explode higher”

as all the talking heads have been prognosticating since (well, technically

since the peak in 1979, but I digress) early this year? It beats me.

But if one was considering making a bullish play in silver, it may be

getting close to time to do so.

My favorite play would be something using

options with a relatively low cost and low dollar risk.

Stay tuned…

See also Jay Kaeppel Interview in July 2020 issue of Technical Analysis of Stocks and Commodities magazine

Disclaimer: The information, opinions and ideas expressed herein are for

informational and educational purposes only and are based on research conducted

and presented solely by the author. The

information presented represents the views of the author only and does not

constitute a complete description of any investment service. In addition, nothing presented herein should

be construed as investment advice, as an advertisement or offering of

investment advisory services, or as an offer to sell or a solicitation to buy

any security. The data presented herein

were obtained from various third-party sources.

While the data is believed to be reliable, no representation is made as

to, and no responsibility, warranty or liability is accepted for the accuracy

or completeness of such information.

International investments are subject to additional risks such as

currency fluctuations, political instability and the potential for illiquid

markets. Past performance is no

guarantee of future results. There is

risk of loss in all trading. Back tested

performance does not represent actual performance and should not be interpreted

as an indication of such performance.

Also, back tested performance results have certain inherent limitations

and differs from actual performance because it is achieved with the benefit of

hindsight.

The

recent “concentration” in the March-August 2020 rally is pretty well

acknowledged at this point. Apple,

Amazon, Facebook, Nvidia, Tesla, Microsoft, growth, momentum, tech, etc. go up

pretty much all the time – everything else, maybe yes, maybe no.

And his kind of ride is great. While it lasts. Now the market is selling off for three days and suddenly everyone wants to know if its time to panic. So, let’s talk “perspective”.

The Here and Now

Since

the Covid panic in February and March, the stock market has staged a historic

rally. The rally has been dominated by

large-cap/growth/tech/momentum stocks.

*September-October:

Anything can happen, so be prepared

*November-April

2021: Based on several seasonal factors plus a lot of bullish momentum signals

I look for a resumption/continuation of the bull market into spring 2021

*May-Oct

2021: Based primarily on seasonal factors, the market could easily struggle

between mid-2021 and mid-2022. But that’s

all a way off and mere prognostication.

For

now, let’s focus on a few obvious trends – trends which may be getting a bit “stretched.”

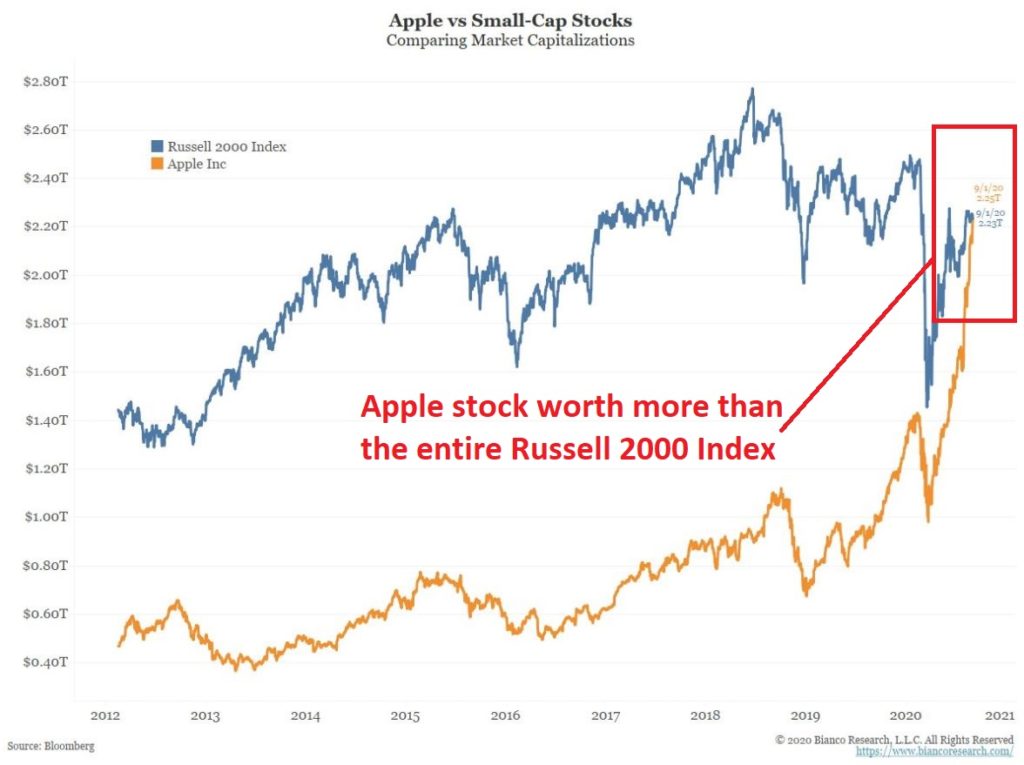

Apple vs. The Little Guy

Figure

1 displays the market capitalization of AAPL versus the ENTIRE Russell 2000

Index.

Figure

1 – Apple vs. Russell 2000 market capitalization (Courtesy: www.BiancoResearch.com)

I am going to give you my perspective as straight as possible. Apple is a great company, it will likely continue to be a great company for a long time, and I have no idea when the price of the stock will top out. All that being said – and even forgetting Apple the company for one second – this type of herd mentality concentration in one asset almost NEVER works out well in the end. The same can be said for Tesla stock market cap dwarfing the rest of the entire automobile industry.

So,

the bottom line:

*Will

AAPL and TSLA stock ultimately rise further?

It wouldn’t surprise me.

*Will

all of this ultimately end badly? Almost

certainly.

*Should

you dump these highfliers now? It beats

me.

*Should

you remain vigilant and be prepared to one day dump these highfliers? Absolutely.

Stock Market Returns vs. Stock Market Valuations

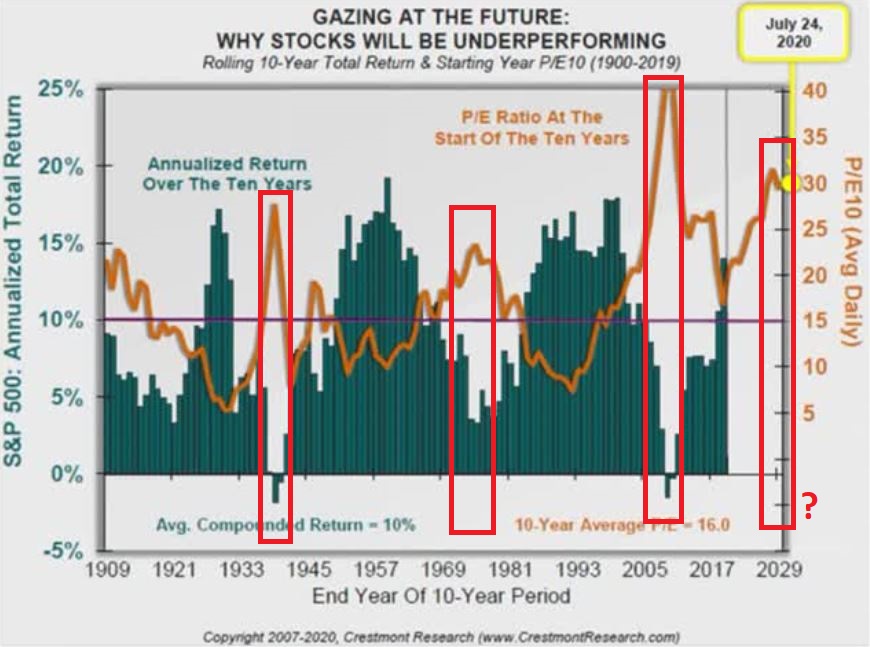

For the record, please note that P/E ratios are lousy timing indicators. The market can remain “overvalued” or “undervalued” for years. BUT, ultimately it does matter. Figure 2 displays the following:

*The

orange line is the P/E ratio at the beginning of a given 10-year period (the

P/E ratio scale is on the right)

*The

bars along the way display the average annual return for the S&P 500 Index

in the subsequent 10 years.

*10-year

periods that start with a high P/E ratio (look for peaks in the orange line)

invariably experience below average 10-year returns

*And

vice versa

*The

current P/E ratio is at the high end of the historical spectrum

What

does it all mean? It likely means that

stock market returns over the next 10 years will NOT resemble the returns in

the past 10 year.

Growth vs. Value

In

recent years “Growth is God” and “Value is Dead”. The difference in performance has not even

been close. So, the longer this goes on

the more it becomes “a given” in the minds of many investors that this trend

will continue ad infinitum. But will

it? History is pretty clear on this

point. With certain relationships

(growth vs. value, large-cap vs. small-cap, U.S. vs. international and so on)

there is a definite ebb and flow over time. Which leads us to:

Jay’s Trading Maxim #45: The only thing more foolish that trying to

time the exact turning point in the ebb and flow of things is believing that a

particular ebb or flow will last forever.

Figure

3 displays 10-year total return for Value versus the 10-year total return for

Growth since the 1930’s. Note that the

current reading is the most extreme reading in favor of growth ever using this

data series.

Figure

3 – 10-year value return minus 10-year growth return (Source: RIA Pro)

While

at the moment the “Growth is God” banner is flying high, Figure 3 argues pretty

strongly that this trend will not last forever.

So, enjoy the growth ride while it lasts, but remember that it will end someday.

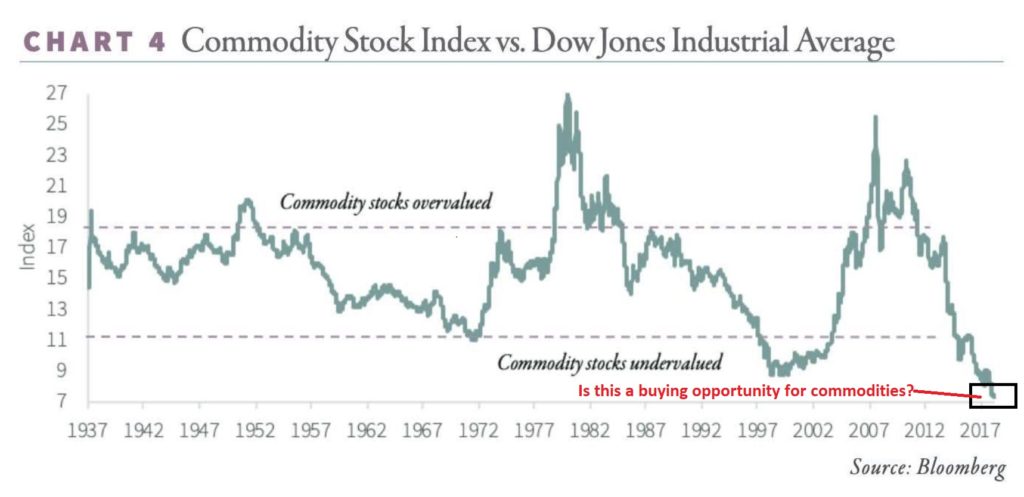

Commodities versus Stocks

Figure

4 displays the relative performance an index of commodity related stocks to the

performance of the S&P 500 Index, going back to the 1930’s. Note that commodity related performance has

never been worse relative to stocks.

Figure

4 – Commodity related stocks versus the S&P 500 Index.

Once

again, trying to pick the exact bottom in this relationship is a mistake. The bigger mistake is assuming this

relationship will never reverse.

Summary

Don’t get caught staring at the “shiny object” for too long. The “large-cap/growth/tech/momentum party will likely resume and roll on for who knows how long. But just remember, all good things gotta come to an end.

See also Jay Kaeppel Interview in July 2020 issue of Technical Analysis of Stocks and Commodities magazine

Disclaimer: The information, opinions and ideas expressed herein are for

informational and educational purposes only and are based on research conducted

and presented solely by the author. The

information presented represents the views of the author only and does not

constitute a complete description of any investment service. In addition, nothing presented herein should

be construed as investment advice, as an advertisement or offering of

investment advisory services, or as an offer to sell or a solicitation to buy

any security. The data presented herein

were obtained from various third-party sources.

While the data is believed to be reliable, no representation is made as

to, and no responsibility, warranty or liability is accepted for the accuracy

or completeness of such information.

International investments are subject to additional risks such as currency

fluctuations, political instability and the potential for illiquid

markets. Past performance is no

guarantee of future results. There is

risk of loss in all trading. Back tested

performance does not represent actual performance and should not be interpreted

as an indication of such performance.

Also, back tested performance results have certain inherent limitations

and differs from actual performance because it is achieved with the benefit of

hindsight.

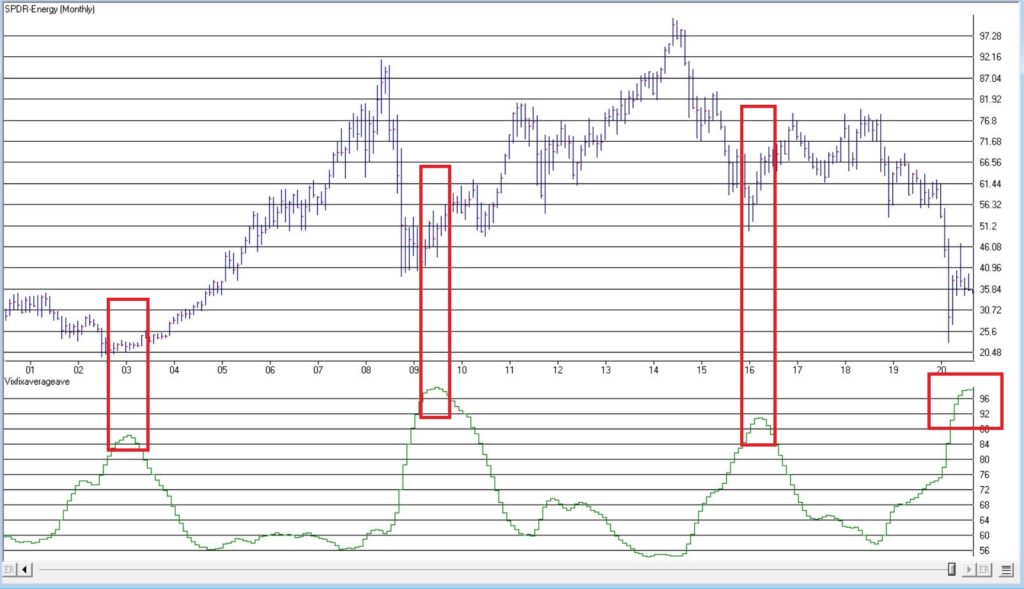

Everyone hates the energy sector (Foreshadowing alert: Well, almost everyone). And a quick perusal of Figure

1 clearly illustrates why the energy sector is unloved.

Since

ticker XLE (Energy Select Sector SPDR ETF) topped out in 2014:

*XLE

has lost -65%

*QQQ

has gained +210%

And

in another kick in the head to the energy sector, Exxon (ticker XOM) was just

kicked out of the Dow Jones Industrial Average.

Take that, losers!

So

yeah, who wouldn’t hate energy stocks and decide to shun them? Well, as it turns out, the answer to that

question of late is “the people who know the energy business the best.”

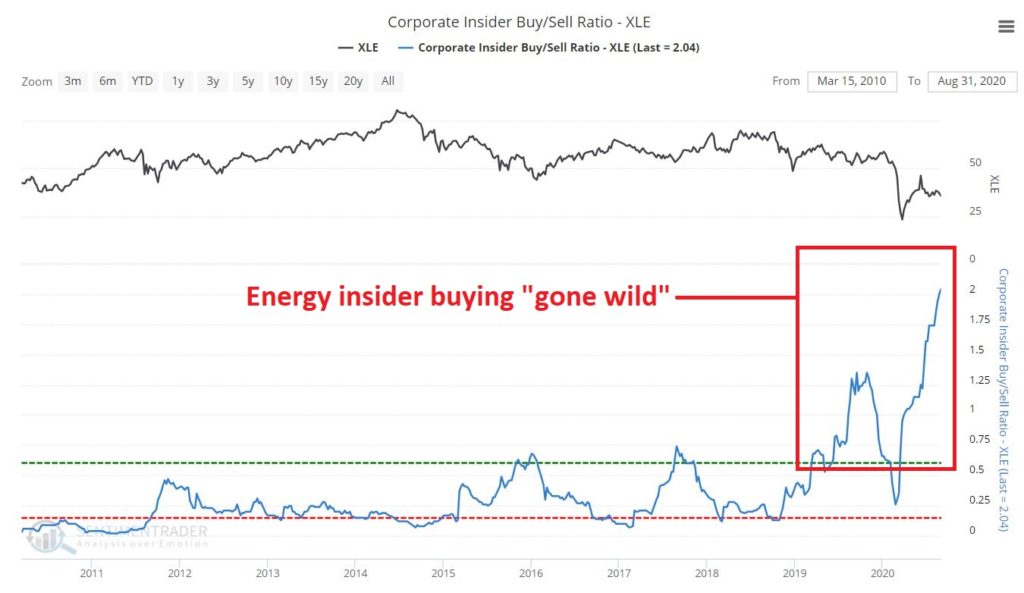

Figure 2 from www.Sentimentrader.com displays the Insider Buy/Sell ratio for executives and other muckety-mucks running energy related corporations. The picture speaks for itself.

As

you can see, energy corporate insiders have been on a massive buying binge of

late. Interestingly, they went on a

buying binge in 2019 – apparently expecting an improvement in the sector – then

the sector got waylaid by Covid-19.

Instead of bailing out the insiders really kicked their share buying into

overdrive as you can see at the far right of Figure 2.

Figure

3 displays ticker XLE with an indicator that I developed by simply smoothing

Larry Williams VixFix indicator. The

gist of the idea, is that when this indicator reaches an extreme high level and

then turns down, it often highlights a “washed out” situation which may be

followed by a bullish move. Ticker XLE

is presently nearing that point.

Should

savvy investors follow the insider’s lead and start piling into the energy

sector? Unfortunately, hindsight is the

only way to know for sure. But for what

it is worth, my own answer is “probably, but maybe not just yet.”

Energy Seasonality

The

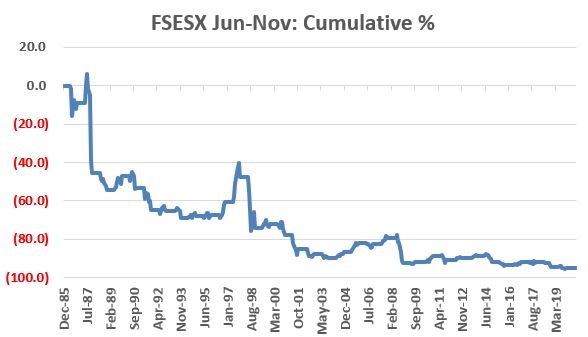

primary reason for hesitation at this exact moment in time is seasonality. Let’s use ticker FSESX (Fidelity Select

Sector Energy Services) as a proxy for the broader energy index. This fund’s first full month of trading was

January 1986. Figure 4 displays the

cumulative total return for ticker FSESX ONLY during the months of June through

November every year since 1986.

Figure

4 – FSESX cumulative % return June through October (1986-2020)

The

cumulative total return during these months for holders of FSESX during June

through November is -94.7%(!!!) So, you

see my hesitation with “piling in”.

Additionally

– climate change concerns aside – much of the energy industry still revolves

around crude oil. Figure 4 displays the

annual seasonal trend by month for crude oil.

Seasonal trends can vary widely from

year-to-year, and there is NO guarantee that trouble lies ahead in Sep-Oct-Nov

for the energy sector.

But that is what history suggests.

Summary

The

bottom line is this:

*Energy

sector corporate insider buying should be seen as a bullish longer-term sign

for the sector

*The

energy sector is so beaten down, battered and unloved that it probably accurate

to refer to the situation as “Blood in the Streets”

Based

on these factors I look for energy to surprise investors in the years

ahead. That being said:

*Trying

to pick the exact bottom in anything is typically a fool’s errand

*Getting bullish on the energy sector in early September is at times fraught with peril.

Sometime around December 1st it will be time to take a close look at the energy sector. If an actual uptrend develops or has already developed, the time may be write for investors to join the insiders.

See also Jay Kaeppel Interviewin

July 2020 issue of Technical Analysis of Stocks and Commodities magazine

Disclaimer: The information, opinions and ideas expressed herein are for

informational and educational purposes only and are based on research conducted

and presented solely by the author. The

information presented represents the views of the author only and does not constitute

a complete description of any investment service. In addition, nothing presented herein should

be construed as investment advice, as an advertisement or offering of

investment advisory services, or as an offer to sell or a solicitation to buy

any security. The data presented herein

were obtained from various third-party sources.

While the data is believed to be reliable, no representation is made as

to, and no responsibility, warranty or liability is accepted for the accuracy

or completeness of such information.

International investments are subject to additional risks such as

currency fluctuations, political instability and the potential for illiquid

markets. Past performance is no

guarantee of future results. There is

risk of loss in all trading. Back tested

performance does not represent actual performance and should not be interpreted

as an indication of such performance.

Also, back tested performance results have certain inherent limitations

and differs from actual performance because it is achieved with the benefit of

hindsight.

One of the keys to trading success is to put as many factors in your favor as possible when identifying a trading opportunity. The other key is to understand that “this time around” those factors may not mean a hill of beans so you had better allocate your capital – and manage your risk – wisely.

A

relevant potential case in point is found in the soybean market.

The Factors: Seasonality

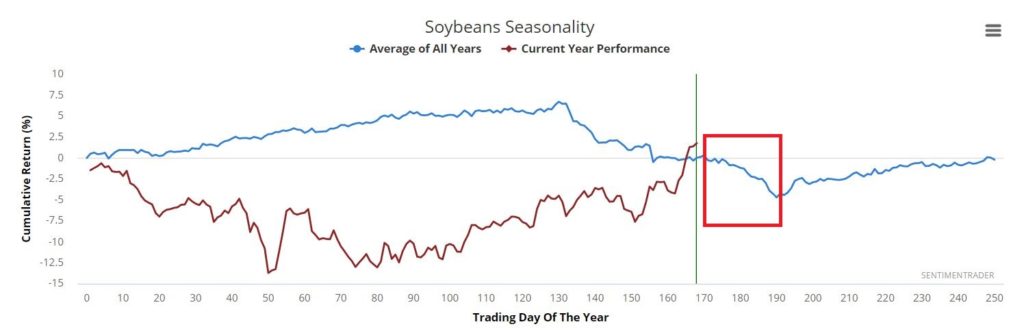

Figure

1 displays the annual seasonal trend for soybeans. Focus on the action of the blue line

contained in the red box.

The

period contained in the box roughly equates to September Trading Day #5 through

October Trading Day #2. We’ll focus on

this period more closely in a moment, but for now just note that seasonality is

suggesting an edge to the bears during this period.

The Factors: Sentiment

Figure 2 displays the Soybeans Optix for the past 10 years. As you can see at the far right, the current Optix value is just touching what would be considered the upper end (i.e., overly bullish sentiment). By itself this should NOT be interpreted as a “Sell Now!!” signal. However, as part of the overall “weight of the evidence” it is fair to add it to the “potentially negative” side of the ledger.

Like

sentiment, the current state of “hedgers positions” on a standalone basis is

not flashing any kind of a definitive signal.

However, it is toward the lower end of the range following a significant

decline in the indicator in the lower clip.

As you can see in Figure 3, previous significant declines in soybean

hedger positions toward roughly a 1-year low have often been followed by

weakness in soybean prices.

What

follows IS NOT a “recommended” trade. It

is simply an example of how a trader might approach this situation, taking this

opportunity into account in terms of:

*Probability

*Capital

allocation

*Risk

control

If

we look a little more closely, we find that the period that extends from the

close on September Trading Day #5 through October Trading Day #2 has been

unfavorable for beans over the year. How

unfavorable?

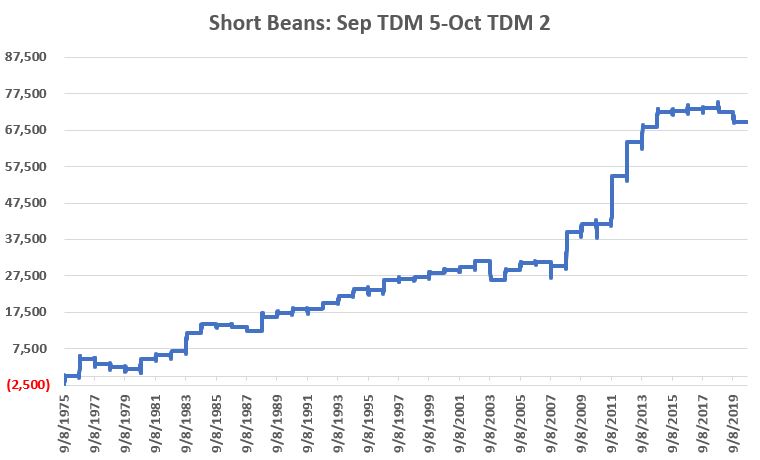

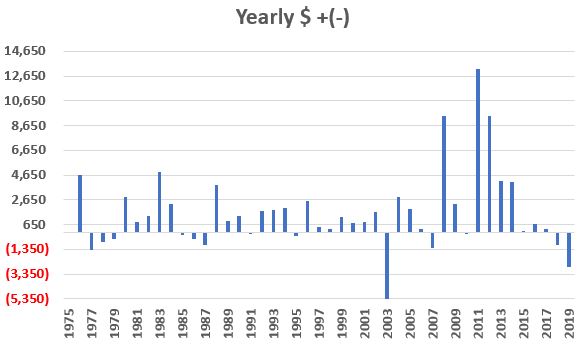

Figure 4 displays the cumulative dollar return from holding a short position in soybeans futures during only this period every year starting in 1975. A price of 950 for soybean futures equates to $9.50 for a bushel of soybeans. Each 1 “point” move is worth $50, so a trader who sells beans at 950 and buys back at 900 earns 50 points times $50 a point, or a gain of +$2.500.

Figure 4 – Soybeans cumulative hypothetical $ +/- holding a short futures position from September Trading Day #5 through October Trading Day #2

Figure 5 displays the yearly $ +(-) hypothetical $ +/- holding a short futures position from September Trading Day #5 through October Trading Day #2

Things to Note:

*32

years showed a gain (71%)

*13

years showed a loss (29%)

*Average

winning trade = +$2,663

*Average

losing trade = (-$1,184)

*Win/Loss

Ratio = 2.46 (71%/29%)

*Ave.

Win/Ave. Loss = 2.25 ($2,663/$1,184)

Clearly

this trend offers possibilities on a “probability” basis.

The

real questions for an actual trader are “how much $ to commit?” and “how much

risk is involved?”

Considering Drawdowns

Figure 6 displays the annual +/- from holding a short position in soybean futures for the full period along with the worst open loss experienced along the way.

Year

$ +(-)

Worst Open $ Loss

1975

$13

($2,425)

1976

$4,625

($475)

1977

($1,425)

($2,250)

1978

($775)

($1,575)

1979

($488)

($1,375)

1980

$2,850

($1,163)

1981

$850

($575)

1982

$1,325

($938)

1983

$4,913

($1,038)

1984

$2,338

($75)

1985

($238)

($1,050)

1986

($513)

($650)

1987

($1,038)

($1,200)

1988

$3,825

$0

1989

$913

$0

1990

$1,300

($450)

1991

($88)

($1,550)

1992

$1,725

$0

1993

$1,850

($338)

1994

$1,988

($225)

1995

($263)

($1,650)

1996

$2,588

($1,038)

1997

$475

($488)

1998

$325

($600)

1999

$1,250

($375)

2000

$800

($50)

2001

$850

($600)

2002

$1,675

($888)

2003

($5,350)

($5,350)

2004

$2,913

$0

2005

$1,900

$0

2006

$275

($500)

2007

($1,288)

($4,550)

2008

$9,400

($650)

2009

$2,300

($1,300)

2010

($138)

($3,875)

2011

$13,200

($450)

2012

$9,400

($1,450)

2013

$4,150

($1,950)

2014

$4,125

$0

2015

$100

($788)

2016

$700

($613)

2017

$275

($1,188)

2018

($1,025)

($1,025)

2019

($2,763)

($3,025)

Figure

6 – Annual hypothetical +/- and largest open loss during life of trade;

1975-2019

To

read Figure 6, in 1975 the short trade registered a net gain of $12.50 (rounded

to $13 in the Table). The worst open

loss during the life of the trade was -$2,425.

In other words, you had to sit through an open loss of -$2,425 in order

to garner the $12.50 profit. As you can

see, these numbers can vary widely from year to year.

Now

let’s get down to the nitty-gritty of capital allocation. First off, there are no hard and fast rules,

so we will simply highlight one common sense approach.

The worst recorded drawdown for any one trade was $5,350 in 2003. As I write, the margin requirement to sell short 1 soybean futures contract at the Chicago Board of Trade is $4,725.

*So, one simple approach would be to add these two values together ($5,350 + $4,725 = $10,075). Using this simple approach, a trader would allocate capital of $10,075 to sell short 1 soybean futures contract.

*IMPORTANT NOTE: A short position in a futures contract entails unlimited risk. So a trader should also consider a stop loss order. There is no “magic number” but for sake of example, let’s assume we want to put a stop-loss beyond the largest previous loss of -$5.350. If we will risk a maximum of $5,400 then we divide $5,400 by $50 and get 108 soybean “points”. So if we sell short a soybean futures contract trading at a quoted price of 965 (or $9.65 a bushel), we might place a stop-loss to buy back the contract at 1,073.

What Kind of Return?

For

sake of example, let’s assume that every year a Trader allocates $10,075 and

sells short 1 soybean futures contract at the close on the 5th

trading day of September and then buys it back to close the short position at

the close on the 2nd trading day of October.

Figure 7 displays the hypothetical annual results in terms of “% return on capital allocated” and “largest open loss as a % of allocated capital.”

Year

% Return

Largest % Open loss

1975

0.1%

(24.1%)

1976

45.9%

(4.7%)

1977

(14.1%)

(22.3%)

1978

(7.7%)

(15.6%)

1979

(4.8%)

(13.6%)

1980

28.3%

(11.5%)

1981

8.4%

(5.7%)

1982

13.2%

(9.3%)

1983

48.8%

(10.3%)

1984

23.2%

(0.7%)

1985

(2.4%)

(10.4%)

1986

(5.1%)

(6.5%)

1987

(10.3%)

(11.9%)

1988

38.0%

0.0

1989

9.1%

0.0

1990

12.9%

(4.5%)

1991

(0.9%)

(15.4%)

1992

17.1%

0.0

1993

18.4%

(3.3%)

1994

19.7%

(2.2%)

1995

(2.6%)

(16.4%)

1996

25.7%

(10.3%)

1997

4.7%

(4.8%)

1998

3.2%

(6.0%)

1999

12.4%

(3.7%)

2000

7.9%

(0.5%)

2001

8.4%

(6.0%)

2002

16.6%

(8.8%)

2003

(53.1%)

(53.1%)

2004

28.9%

0.0

2005

18.9%

0.0

2006

2.7%

(5.0%)

2007

(12.8%)

(45.2%)

2008

93.3%

(6.5%)

2009

22.8%

(12.9%)

2010

(1.4%)

(38.5%)

2011

131.0%

(4.5%)

2012

93.3%

(14.4%)

2013

41.2%

(19.4%)

2014

40.9%

0.0

2015

1.0%

(7.8%)

2016

6.9%

(6.1%)

2017

2.7%

(11.8%)

2018

(10.2%)

(10.2%)

2019

(27.4%)

(30.0%)

Average

+15.4%

(-11.0%)

Figure

7 – % returns and risks

Summary

Will soybeans decline between the close on 9/8/2020 and 10/2/2020? It beats me. This seasonal trade has been a loser each of the last two years and seasonality overall has not been great in 2020.

Still history clearly suggests a negative bias. When we add in sentiment and hedgers positioning, the odds seem to favor a the downside. In the end – and as always – the real questions are “how much money do you have to commit” and “is it worth the risk” in your opinion.

See also Jay Kaeppel Interview in July 2020 issue of Technical Analysis of Stocks and Commodities magazine

Disclaimer: The information, opinions and ideas expressed herein are for

informational and educational purposes only and are based on research conducted

and presented solely by the author. The

information presented represents the views of the author only and does not constitute

a complete description of any investment service. In addition, nothing presented herein should

be construed as investment advice, as an advertisement or offering of

investment advisory services, or as an offer to sell or a solicitation to buy

any security. The data presented herein

were obtained from various third-party sources.

While the data is believed to be reliable, no representation is made as

to, and no responsibility, warranty or liability is accepted for the accuracy

or completeness of such information.

International investments are subject to additional risks such as

currency fluctuations, political instability and the potential for illiquid

markets. Past performance is no

guarantee of future results. There is

risk of loss in all trading. Back tested

performance does not represent actual performance and should not be interpreted

as an indication of such performance.

Also, back tested performance results have certain inherent limitations

and differs from actual performance because it is achieved with the benefit of

hindsight.

Maybe

not even consciously in many cases (think of any cash you have anywhere – checking,

savings, money-market, brokerage account but not invested in anything at the

moment, etc.), but most investors are “earning interest” on some portion of

their assets. Not much interest. Not in the current “low interest rate environment”,

but interest nevertheless.

Yet

the interesting (har) thing is that the vast majority of investors never think

about how changes in interest rates affect things. For our example, we will go to the far end of

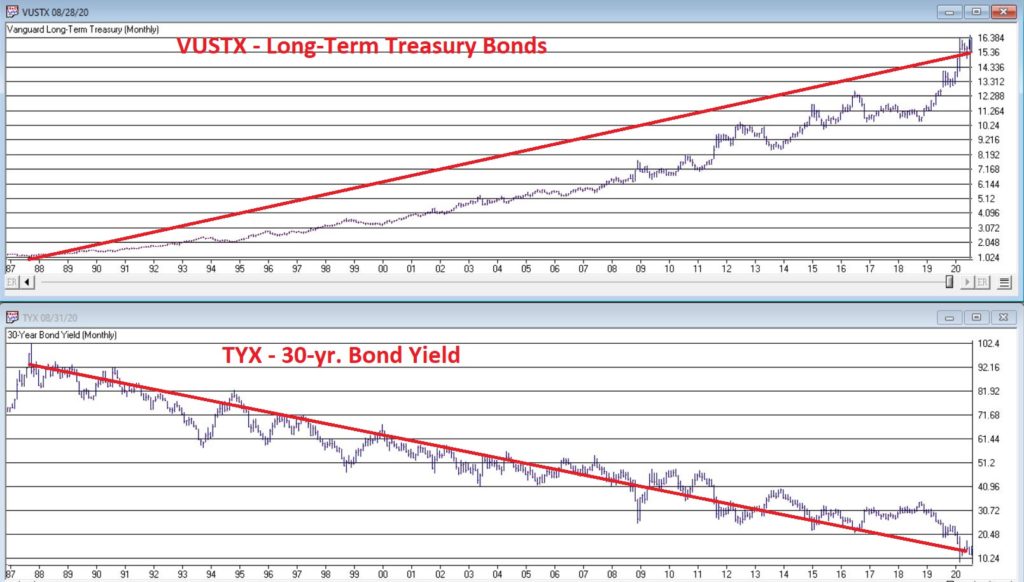

the bond spectrum – the 30-year treasury bond.

Long-term treasuries are essentially the “purest play” on interest rates

because treasury bonds are assumed to entail no “credit risk”, they trade

solely based on “interest rate risk”, i.e.:

*When

long-term interest rates go DOWN, long-term treasury price go UP

*When

long-term interest rates go UP, long-term treasury price go DOWN

Figure

1 “says” it all. The top clip is price

action for ticker VUSTX (Vanguard Long-Term Treasury) and the bottom clip is

ticker $TYX (an index that tracks the yield on 30-year treasuries times 10 – so

if TYX is at 20, it means the yield on LT treasuries is 2%).

The

obvious thing to note is the inverse relationship.

The 2 Big Questions

The

“2 Big Questions” in this example are:

*Where

will long-term interest rates go from here?

*What

will happen to long-term treasury bonds as a result?

Interestingly,

the answers are:

“No

one really knows for sure”

“We

can calculate it almost exactly”

There

is lots of speculation regarding where interest rates will go from here. One camp says the Fed will keep forcing rates

lower – possibly even into negative territory (it has already happened in other

parts of the world, and “Yes”, it can happen here).

The

other camp argues that all the money printing will spark inflation and that

will lead to higher rates.

Again, no one knows for sure. Fortunately, the one thing we can do – with only the help of a handy bond calculator – is figure out how long-term treasury bond prices will react.

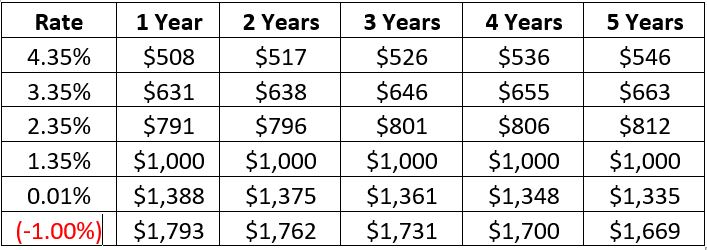

An Example

Let’s

assume a new 30-year treasury bond is issued today with a yield of 1.35%. These means:

*Buyer

pays $1,000 to buy the bond

*Every

year for the next 30 years the treasury pays bondholder $135 in interest

*In

30 years, the treasury pays the bondholder back the original $1,000

The

calculations below estimate the expected change in price and $ value of a

30-year treasury bond based on interest rate movement and the passage of time.

NOTE: The data in the tables “may not compute” in your head at

first. If not, I strongly encourage you

to step back and then take another shot.

Because this data spells out the potential risks and rewards pretty

explicitly.

Figure

2 displays the expected dollar value of a current 30-year treasury 1 to 5 years

from now based on some future level of interest rates.

Figure 3 displays the expected percentage change in dollar value of a current 30-year treasury 1 to 5 years from now based on some future level of interest rates.

Figure 2 – Expected $ Value of 30-year 1.35% bond based on change in current interest rate and the passage of time

Figure 3 – Expected % change in price of 30-year 1.35% bond based on change in current interest rate and the passage of time

So,

let’s use the extremes as examples:

*If

rates fall to -1.00% one year from now, today’s 30-year treasury will rise in

value from $1,000 to $1,793 or +79%

*If

rates rise to 4.35% five years from now, today’s 30-year treasury will be

priced at $546, or -45% below today’s price level.

What It All Means

First

off note that investments in shorter-term securities will have less volatility

in terms of price movement, but will still be affected by changes in rates.

If interest rates rise:

*Bond

holders – especially holders of long-term bonds – will get hurt.

*As

you can see in Figures 2 and 3, if rates were to rise over the next several

years long-term bonds would be severely underwater and could take as long as

waiting until maturity to get back to $1,000 in value.

If interest rates fall:

*Bond

holders can still profit significantly.

*If

the bottom fell out of interest rates and they plunged to -1.00% a year from

now, our 30-year treasury bond would gain a massive +79%.

BUT

BEWARE: Remember – even if rates did fall to -1.00% a year from now, and if our

30-year bond soared in value to $1,793 a year from now – ultimately our 30-year

bond is going to mature at a value of $1,000.

So, any gains above that value would eventually evaporate.

To

spell it out: If interest rates do decline towards 0% or even below, hitting

the “Sell” button would likely make sense at some point.

See also Jay Kaeppel Interviewin

July 2020 issue of Technical Analysis of Stocks and Commodities magazine

Disclaimer: The information, opinions and ideas expressed herein are for

informational and educational purposes only and are based on research conducted

and presented solely by the author. The

information presented represents the views of the author only and does not

constitute a complete description of any investment service. In addition, nothing presented herein should

be construed as investment advice, as an advertisement or offering of

investment advisory services, or as an offer to sell or a solicitation to buy

any security. The data presented herein

were obtained from various third-party sources.

While the data is believed to be reliable, no representation is made as

to, and no responsibility, warranty or liability is accepted for the accuracy

or completeness of such information.

International investments are subject to additional risks such as

currency fluctuations, political instability and the potential for illiquid

markets. Past performance is no

guarantee of future results. There is

risk of loss in all trading. Back tested

performance does not represent actual performance and should not be interpreted

as an indication of such performance.

Also, back tested performance results have certain inherent limitations

and differs from actual performance because it is achieved with the benefit of

hindsight.