As of January 1st, 2021, I will be joining www.Sentimentrader.com. I have long been a fan, a follower and a user of this top website. Founded by Jason Goepfert, I have long considered Sentimentrader to be the leader in quantitative market analysis. When I was offered the opportunity to join the team I jumped at the chance.

Needless to say, I encourage everyone

to consider subscribing and to take advantage of the wealth of information

contained on the site (that I have used for years) as well as the straightforward,

objective analysis that is offered on a daily basis.

I plan to bring a lot of previously

unreleased material with me and as much insight as I can muster on the topics

of trading systems/strategies, seasonality, options trading and on how to “think

like a trader.”

Wishing you all a Happy New Year!

Jay

Kaeppel

Disclaimer: The information, opinions and ideas expressed herein are for

informational and educational purposes only and are based on research conducted

and presented solely by the author. The

information presented represents the views of the author only and does not

constitute a complete description of any investment service. In addition, nothing presented herein should

be construed as investment advice, as an advertisement or offering of

investment advisory services, or as an offer to sell or a solicitation to buy

any security. The data presented herein

were obtained from various third-party sources.

While the data is believed to be reliable, no representation is made as

to, and no responsibility, warranty or liability is accepted for the accuracy

or completeness of such information.

International investments are subject to additional risks such as

currency fluctuations, political instability and the potential for illiquid

markets. Past performance is no

guarantee of future results. There is

risk of loss in all trading. Back tested

performance does not represent actual performance and should not be interpreted

as an indication of such performance.

Also, back tested performance results have certain inherent limitations

and differs from actual performance because it is achieved with the benefit of

hindsight.

I plan to bring a lot of material and as much insight as I can muster on the topics of trading systems/strategies, seasonality, options trading and on how to “think like a trader.”

Wishing you all a Happy New Year!

See also Jay Kaeppel Interview in July 2020 issue of Technical Analysis of Stocks and Commodities magazine

Disclaimer: The information, opinions and ideas expressed herein are for

informational and educational purposes only and are based on research conducted

and presented solely by the author. The

information presented represents the views of the author only and does not

constitute a complete description of any investment service. In addition, nothing presented herein should

be construed as investment advice, as an advertisement or offering of

investment advisory services, or as an offer to sell or a solicitation to buy

any security. The data presented herein

were obtained from various third-party sources.

While the data is believed to be reliable, no representation is made as

to, and no responsibility, warranty or liability is accepted for the accuracy

or completeness of such information.

International investments are subject to additional risks such as

currency fluctuations, political instability and the potential for illiquid

markets. Past performance is no

guarantee of future results. There is

risk of loss in all trading. Back tested

performance does not represent actual performance and should not be interpreted

as an indication of such performance.

Also, back tested performance results have certain inherent limitations

and differs from actual performance because it is achieved with the benefit of

hindsight.

The trend is your friend. At least until it is not a trend

anymore. Then it becomes more like an ex

who keeps trying to “lure you back in” with memories of “the good times”, even

though the relationship has unquestionably run its course. In both cases the end is pretty similar.

Investors have been blessed with a

variety of strong and persistent trends in recent years. By getting onboard and staying onboard many

investors have been able to accumulate a great deal of wealth.

But nothing – particularly a trend in

the financial markets – lasts forever. I

(nor anyone else) cannot predict when any particular trend or relationship in

the markets will end. But the one thing

we can do is recognize when a trend or relationship is “getting a little long

in the tooth” and prepare ourselves mentally for the day when we need to walk

(or run, as the case may be) away.

5 Relationships to Watch

I am on the record as believing that

the next 5-10 years in the markets will look much different than the last 10

years. For example, I expect:

*Foreign stocks to outperform U.S.

stocks

*Value to outperform growth

*Commodities to outperform stocks

*Technology to suffer a severe bear

market

*Energy stocks to some day rise from

the dead

Interestingly, I have very little money committed to most of these ideas at the moment. Lacking “courage of conviction?” OK, I don’t claim to be immune. But in this case, it is more a function of the belief that “it’s not so much what you buy but when you buy it that matters.”

And long ago I gave up trying to pick

tops and bottoms. So, for the moment I

am watching and waiting for “signs.” Let

me show you some charts you can use to make your own determination.

Each of the charts below are “relative

strength” charts, NOT price charts. In

other words, the chart displays how one asset is performing relative to

another.

*If the bars in the chart are rising

it means the 1st asset listed is outperforming

*If the bars in the chart are

declining it means the 1st asset listed in underperforming

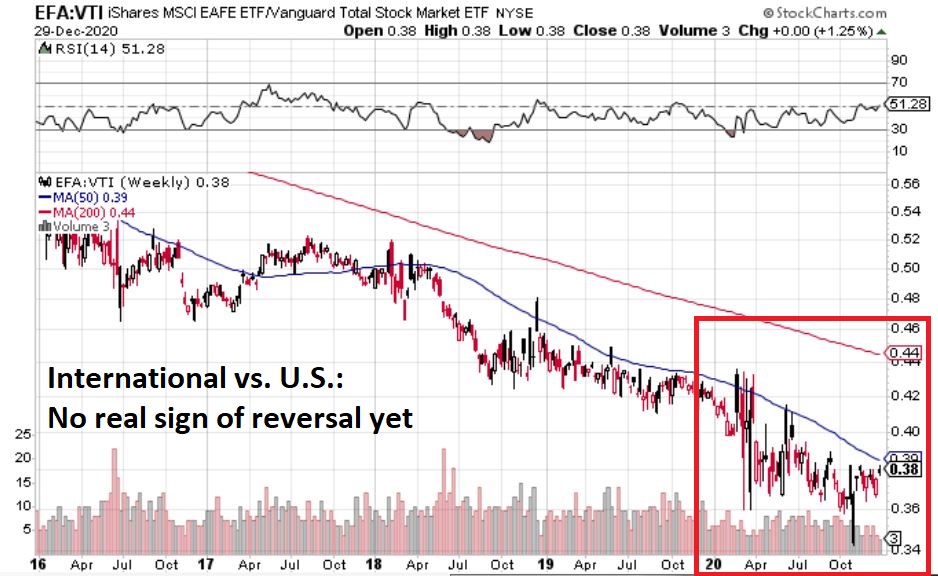

#1. Foreign stocks versus U.S. stocks

Figure 1 displays a weekly chart of

the performance of ticker EFA (iShares MSCI EAFE Index ETF) relative to ticker

VTI (Vanguard Total U.S. Stock Market ETF).

The downward slope illustrates the

fact that U.S. stocks have consistently outperformed in recent years. In addition, there is little sign of a

turnaround yet.

Figure 1 – EFA vs. VTI (Foreign vs. U.S)

#2. Value vs. Growth

Figure 2 displays a weekly chart of

the performance of ticker VTV (Vanguard Value ETF) relative to ticker VUG (Vanguard

Growth ETF).

The downward slope illustrates the

fact that growth stocks have vastly outperformed value stocks in recent

years. My “opinion” is that value will

almost certainly outperform growth in the decade ahead – and yet I have not

committed any money to value funds or ETFs yet.

Why? There is little sign of a

turnaround in Figure 2 yet.

Figure 2 – VTV vs. VUG (Value vs. Growth)

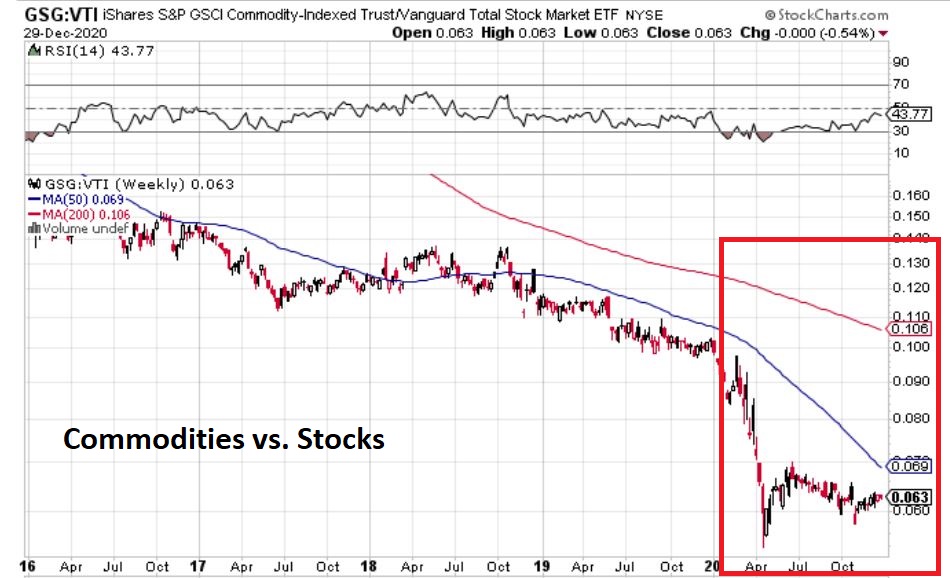

#3. Commodities vs. Stocks

Figure 3 displays a weekly chart of

the performance of ticker GSG (Goldman Sachs Commodity Index ETF) relative to

ticker VTI (Vanguard Total U.S. Market ETF).

My “opinion” here is that commodities

likely represent generational opportunity to “buy cheap”. A number of commodities (Gold, soybeans, lithium,

lumber, copper) have already started to rally, but commodities as an asset

class have not realty outperformed the stock market following the stock market

low in March.

But keep a close eye on Figure 3 for

some sign of a turnaround.

Figure 3 – GSG vs. VTI (Commodities vs. Stocks)

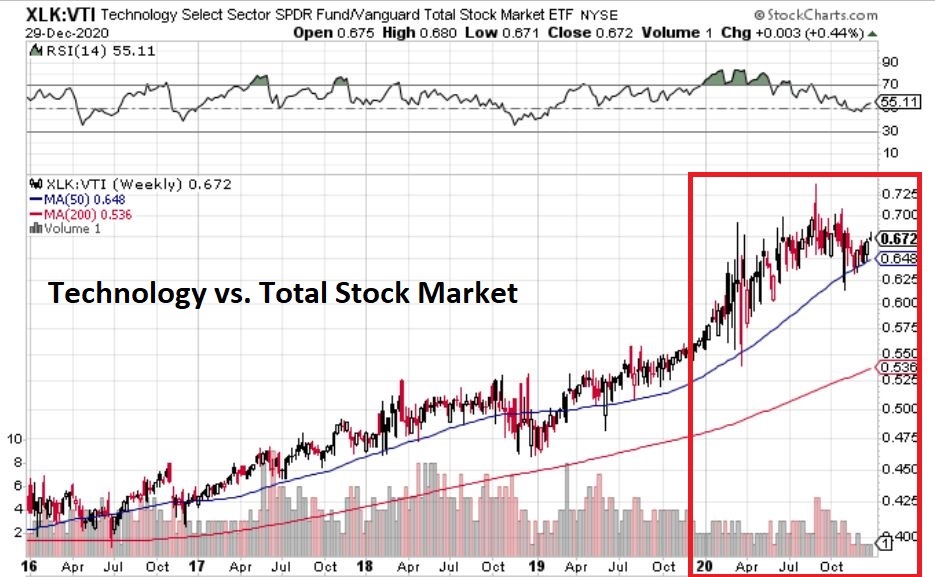

#4. Technology Sector vs. The Total

Stock Market

It is no secret that the tech sector has been the strongest performing sector in each of the last two years. Jason Goepfert at www.Sentimentrader.com wrote a Members Only piece the other day that:

*Identified prior instances when one

sector led everything 2 years in a row

*Highlighted how that sector performed

going forward.

Summarizing as succinctly as possible

without violating any copyrights, “it’s not good.” Which raises an interesting reminder of “how

investor’s minds work.” At this moment

in time, it is pretty much accepted wisdom that “tech is where it’s at” and

that that’s how it is going to be ad infinitum into the future. And yes, technology will continue to evolve

at a rapid pace. But must I remind

everyone that “stock prices fluctuate” (or than AAPL lost -91% in 2000-2002 and

AMZN lost -95% and GOOG lost -97%)? I am

not “predicting” a repeat, but I am very alert to the fact that tech stocks are

“due” for a whack.

Will that happen in 2021? It beats me.

But I will be keeping a close eye on Figure 4 that displays ticker XLK

(SPDR Technology) vs. ticker VTI (Vanguard Total U.S. Market ETF). Enjoy the ride for now because it could

develop into a blowoff top kind of rally.

But whenever this relationship starts to breakdown, run, don’t walk to

the nearest exit.

Figure 4 – XLK vs. VTI (Technology vs. Total U.S. Stock Market)

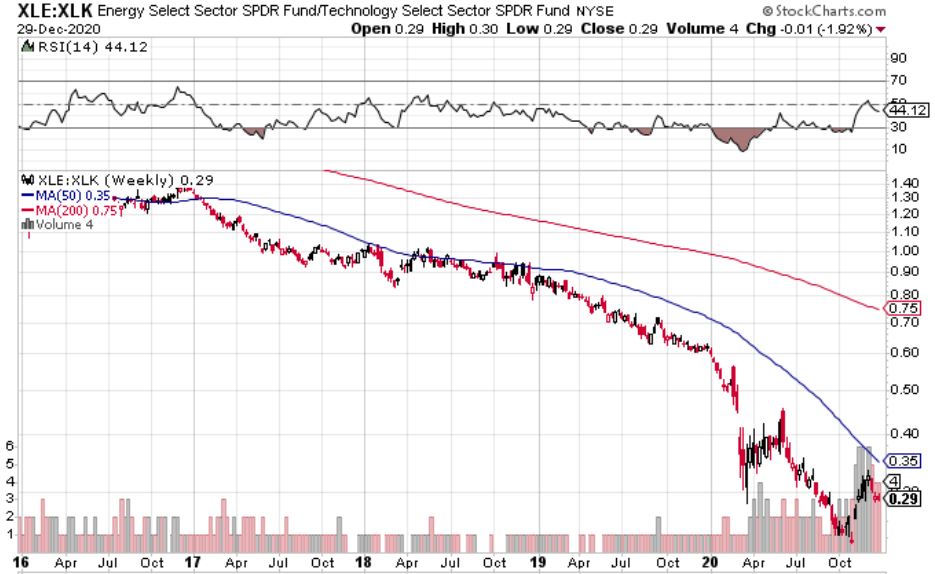

#5. Energy Stocks vs. Technology

Stocks

Figure 5 displays a weekly chart of the performance of ticker XLE (SPDR Energy) relative to ticker XLK (SPDR Technology).

The relative performance between two

sectors has rarely if ever been more one sided. While technology led the

universe in recent years, traditional energy stocks have cratered. There is a part of me that things that traditional

energy stocks also represent a generational opportunity. But there is some doubt:

*On one hand, by and large the world

(particularly transportation and particularly flight) still runs on fossil

fuels. And roughly 10 bazillion products

that we use every day are produced using petroleum. So, one can argue that this sector has been

overdone to the downside and now represents great value.

*On the other hand, the drive to move

to “green energy” is not likely to abate.

Figure 5 – XLE vs. XLK (Energy vs. Technology)

You may never see a more one-sided relative performance than this one. While technology led the universe by far in recent years, traditional energy stocks have cratered. There is a part of me that things that traditional energy stocks also represent a generational opportunity. But there is some doubt:

*On one hand, by and large the world

(particularly transportation and particularly flight) still runs on fossil

fuels. And roughly 10 bazillion products

that we use every day are produced using petroleum. So, one can argue that this sector has been

overdone to the downside and now represents great value.

*On the other hand, the drive to move to “green energy” is not likely to abate.

One possibility might be to focus on green energy companies instead of fossil fuel related. Ironically, stocks in the “green energy” sector have performed so well in recent months that they seem a little “overdone” at the moment.

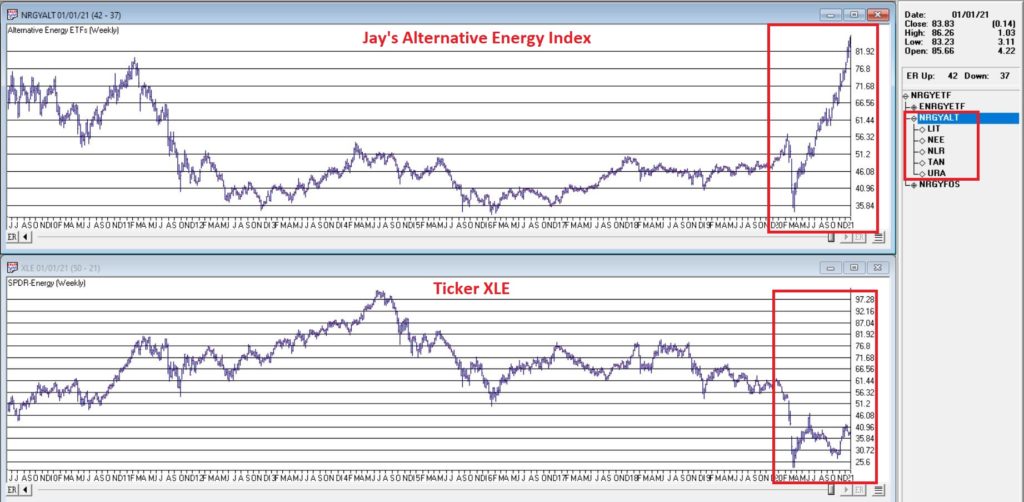

Bonus Chart: “Alternative Energy”

Index versus XLE

Figure 6 displays my own “Alternative

Energy” Index in the top clip and ticker XLE (which is comprised of more

traditional fossil fuel-based companies).

Figure 6 – Alternative Energy Index

vs. Ticker XLE

The differences in recent months are

fairly obvious. So, should one seek “value”

in traditional energy? Or chase

performance with alternative energy?

Just one more thing to keep an eye on

as 2021 dawns.

See also Jay Kaeppel Interview in July 2020 issue of Technical Analysis of Stocks and Commodities magazine

Jay

KaeppelDisclaimer: The information, opinions and ideas expressed

herein are for informational and educational purposes only and are based on

research conducted and presented solely by the author. The information presented represents the

views of the author only and does not constitute a complete description of any

investment service. In addition, nothing

presented herein should be construed as investment advice, as an advertisement

or offering of investment advisory services, or as an offer to sell or a

solicitation to buy any security. The

data presented herein were obtained from various third-party sources. While the data is believed to be reliable, no

representation is made as to, and no responsibility, warranty or liability is

accepted for the accuracy or completeness of such information. International investments are subject to

additional risks such as currency fluctuations, political instability and the

potential for illiquid markets. Past

performance is no guarantee of future results.

There is risk of loss in all trading.

Back tested performance does not represent actual performance and should

not be interpreted as an indication of such performance. Also, back tested performance results have

certain inherent limitations and

And that is true if one looks at

things on a calendar month basis. In

this piece however, we are going to “cut things a little finer.”

Favorable Period for Platinum

For purposes of this piece, we will

define the “Favorable Period” for platinum as:

*The 41 trading days (NOT calendar

days) directly after the 13th trading day of December

Technically this period in 2020

started at the close on 12/17/20 and will extend through the close of trading

on 2/18/2021.

So far in 2020 it is “so far, not so

good”. From the 12/17 close through the

12/24 close platinum has declined from roughly $1,054 and ounce to roughly

$1,027.

So, does this mean that “it is not

working this time around”? Or do we have

a better buying opportunity now than we did on 12/17? The reality is that I can’t answer those

questions. All I can do is highlight the

history and let everyone else make up their own mind.

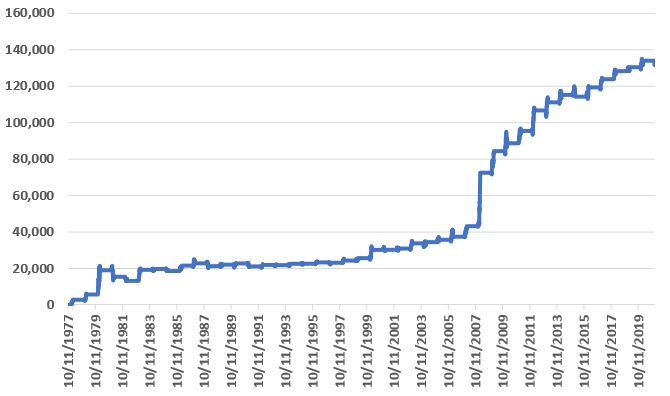

The History

I have platinum futures historical

data going back to October of 1977. So,

we start our test in December 1977 and assume that a trader held a 1-lot of

platinum futures (more on an ETF alternative later) every year during the “favorable

period” defined above. Each full point

movement for a platinum futures contract equals $50. So, if platinum futures advanced 10 points

then the trader gains $500 and vice versa.

Figure 2 displays the cumulative hypothetical

$ +(-) achieved by holding platinum ONLY during the favorable 41-day period

every year.

Figure 2 – Cumulative $ +(-) for

holding 1-lot of platinum futures during 41-day Favorable Period every year

(1978-2020)

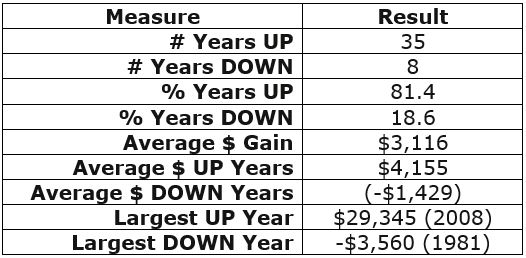

Figure 3 displays some relevant facts

and figures.

Figure 3 – Facts and Figures

As you can see in Figures 2 and 3:

*This favorable 41 trading day period

is “no sure thing”

*However, if you were going to bet on

a direction during this period, the bullish side appears to be the better bet

An ETF Alternative

While the above is all very

interesting on a theoretical basis, the reality is that a very low percentage

of traders will ever touch a platinum futures contract (or should ever touch a

platinum futures contract, given the inherent associated risks).

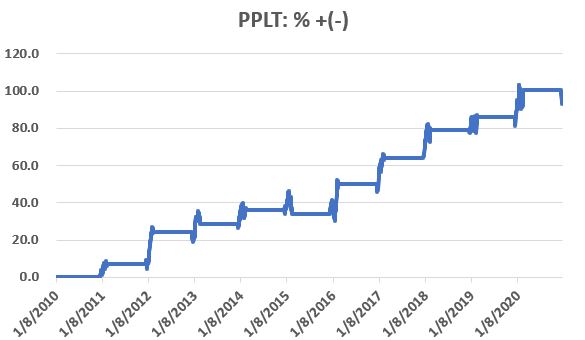

One alternative is to trade shares of

ticker PPLT (Aberdeen Standard Physical Platinum Shares ETF). Figure 4 displays the cumulative hypothetical

price return for PPLT ONLY during the 41-day favorable period since the ETF was

created in 2010.

Figure 4 – Cumulative % + (-) for

ticker PPLT during Favorable Period

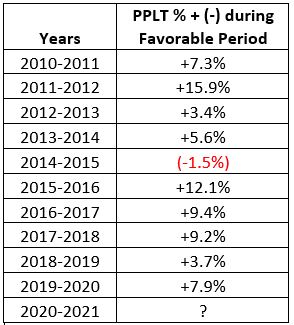

Figure 5 displays the year-by-year results

for PPLT during the Favorable Period.

Figure 5 – PPLT %+(-) year-by-year

during Favorable Period

During the 1st five trading days of this years “Favorable Period”, PPLT has declined -1.8%.

Summary

The good news about seasonal trends

is that they can often afford you an “edge” in the markets. The bad news about seasonal trends is that

you never know if a given trend will play out as expected “this time around” –

so a certain leap of faith is required.

One’s choices regarding platinum

between now and 2/28/2021 are:

*Bet a lot

*Bet a little

*Bet nothing at all

Choose wisely.

See also Jay Kaeppel Interview in July 2020 issue of Technical Analysis of Stocks and Commodities magazine

Disclaimer: The information, opinions and ideas expressed herein are for

informational and educational purposes only and are based on research conducted

and presented solely by the author. The

information presented represents the views of the author only and does not

constitute a complete description of any investment service. In addition, nothing presented herein should

be construed as investment advice, as an advertisement or offering of

investment advisory services, or as an offer to sell or a solicitation to buy

any security. The data presented herein

were obtained from various third-party sources.

While the data is believed to be reliable, no representation is made as

to, and no responsibility, warranty or liability is accepted for the accuracy

or completeness of such information.

International investments are subject to additional risks such as

currency fluctuations, political instability and the potential for illiquid

markets. Past performance is no

guarantee of future results. There is

risk of loss in all trading. Back tested

performance does not represent actual performance and should not be interpreted

as an indication of such performance.

Also, back tested performance results have certain inherent limitations

and differs from actual performance because it is achieved with the benefit of

hindsight.

A strong argument can be made that it’s not “what you buy” but “when you buy it” that matters most. Certainly not every trader would agree with that statement (which is a good thing otherwise we would have no one to trade with). But with this thought in mind, let’s jump ahead and take a brief look into 2021.

2021: By the Calendar

As it fits into the 4-year election

cycle 2021 is a “post-election” year.

Post-election years have a reputation as being “unfavorable” for the

stock market. In reality, they are

“about average” for the stock market. If

we look at price only performance for the Dow Industrial Average every

post-election starting in 1901, we find:

*16 times up, 14 times down – a 53.3%

win rate

*Average % gain = +6.8%

Now let’s break the post-election

year down a little finer:

*”Favorable” period = March, April, May, July and December

*”Unfavorable” period = All other months

The Test

So let’s look at the cumulative

returns one might have achieved if a person (had lived to be a very ripe old age,

and);

*Held the Dow ONLY during the

“Favorable” months

OR

*Held the Dow ONLY during “all other

months”

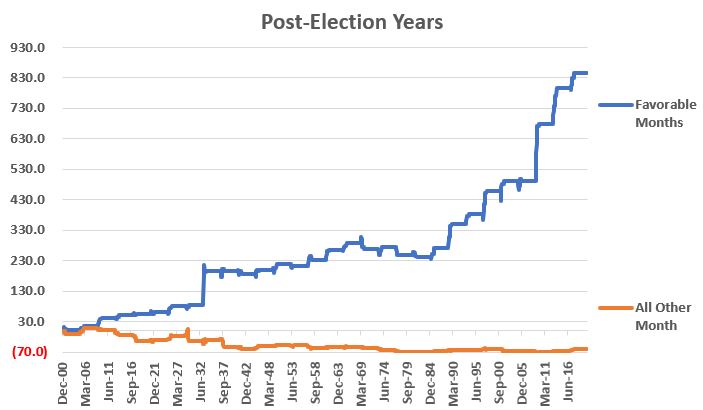

The blue line in Figure 1 displays the cumulative growth achieved ONLY during the “favorable” post-election year months of March, April, May, July and December.

The orange line displays the

cumulative growth achieved only during “all other” post-election months.

Figure 1 – Post-Election Years “Favorable Months” cumulative price gain (blue) versus “All Other Months” cumulative price gain (orange); 1901-present

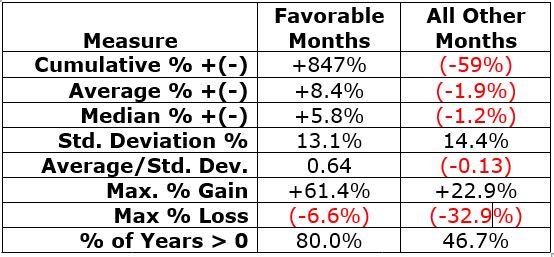

Figure 2 displays the relevant facts and figures.

Figure 2 – Post-Election Years “Favorable Months” versus “All Other Months”; 1901-present

The key things to note:

*The “favorable months” achieved a cumulative return of +847%; the “unfavorable months” achieved a loss of -59%

*The “favorable months” showed an annual gain 80% of the time (versus 53% for buy and hold and 47% for “all other months”)

*The average and median results for “favorable months” were positive, while the average and median results for “all other months” were negative.

*The worst annual loss achieved during “favorable months” only was -6.6%. The worst annual loss for “all other months” was -32.9%

Summary

Post-election years have seen the Dow

gain 53% of the time since 1901 for a cumulative price gain of +286%.

However, a trader who held the Dow ONLY

during April, May, July and December of each post-election year enjoyed an “Up”

post-election year 80% of the time with a cumulative price gain of +640%.

Is this “edge” guaranteed to play out

in 2021? Not at all. But it might be worth remembering.

See alsoJay Kaeppel Interview in July 2020 issue of Technical Analysis of Stocks and Commodities magazine

Disclaimer: The information, opinions and ideas expressed herein are for

informational and educational purposes only and are based on research conducted

and presented solely by the author. The

information presented represents the views of the author only and does not

constitute a complete description of any investment service. In addition, nothing presented herein should

be construed as investment advice, as an advertisement or offering of

investment advisory services, or as an offer to sell or a solicitation to buy

any security. The data presented herein

were obtained from various third-party sources.

While the data is believed to be reliable, no representation is made as

to, and no responsibility, warranty or liability is accepted for the accuracy

or completeness of such information.

International investments are subject to additional risks such as

currency fluctuations, political instability and the potential for illiquid

markets. Past performance is no

guarantee of future results. There is

risk of loss in all trading. Back tested

performance does not represent actual performance and should not be interpreted

as an indication of such performance.

Also, back tested performance results have certain inherent limitations

and differs from actual performance because it is achieved with the benefit of

hindsight.

In many ways the markets imitate

life. For example, the trend is your

friend. You may enjoy your friendship

with the trend for an indefinite length of time. But the moment you ignore it – or just simply

take it for granted that this friendship is permanent, with no additional effort

required on your part – that’s when the trouble starts.

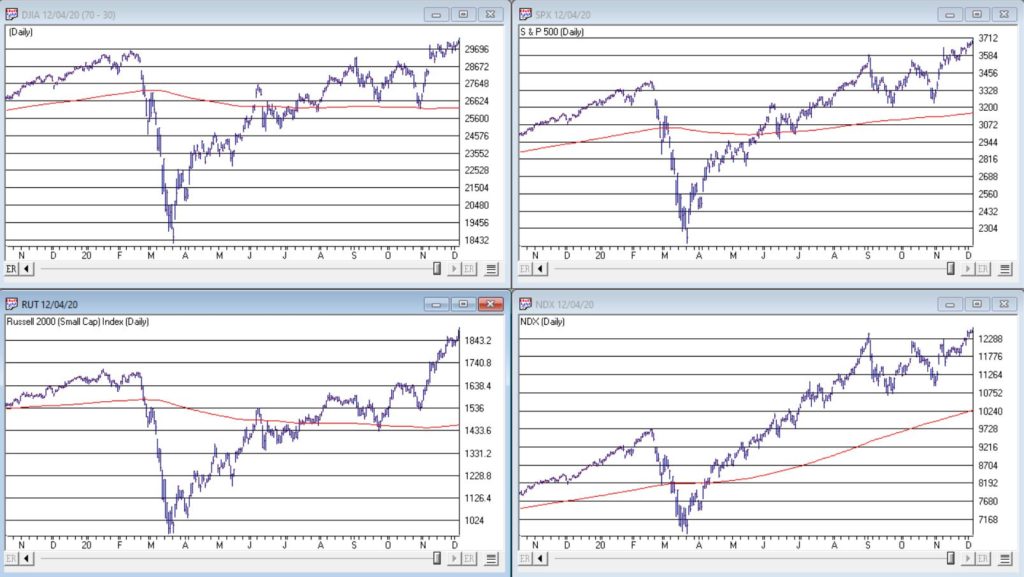

For the stock market right now, the bullish trend is our friend. Figure 1 displays the 4 major indexes all above their respective – and rising – long-term moving averages. This is essentially the definition of a “bull market.”

In addition, a number of indicators

that I follow have given bullish signals in the last 1 to 8 months. These often remain bullish for up to a

year. So, for the record, with my

trusted trend-following, oversold/thrust and seasonal indicators mostly all

bullish I really have no choice but to be in the bullish camp.

Not that I am complaining mind you. But like everyone else, I try to keep my eyes open for potential signs of trouble. And of course, there are always some. One of the keys to long-term success in the stock market is determining when is the proper time to actually pay attention to the “scary stuff.” Because scary stuff can be way early or in other cases can turn out to be not that scary at all when you look a little closer.

So, let’s take a closer look at some

of the scary stuff.

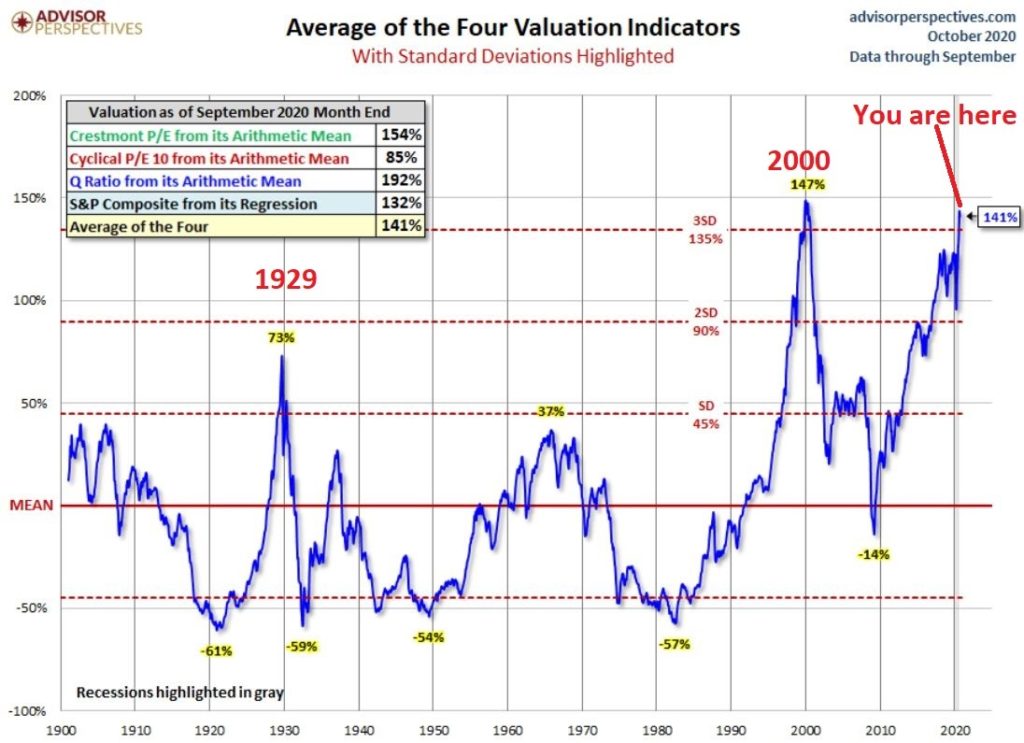

Valuations

Figure 2 displays an aggregate model

of four separate measures of valuation.

The intent is to gain some perspective as to whether stocks are overvalued,

undervalued or somewhere in between.

Clearly the stock market is “overvalued” if looked at from a historical perspective. The only two higher readings preceded the tops in 1929 (the Dow subsequently lost -89% of its value during the Great Depression) and 2000 (the Nasdaq 100 subsequently lost -83% of its value).

Does this one matter? Absolutely. But here is what you need to know:

*Valuation IS NOT a timing indicator. Since breaking out to a new high in 1995 the

stock market has spent most of the past 25 years in “overvalued” territory. During this time the Dow Industrials have

increased 700%. So, the proper response

at the first sign of overvaluation should NOT be “SELL.”

*However, ultimately valuation DOES matter.

Which leads directly to:

Jay’s Trading Maxim #44: If you are walking down the street and you trip and fall that’s one thing. If you are climbing a mountain and you trip and fall that is something else. And if you are gazing at the stars and don’t even realize that you are climbing a mountain and trip and fall – the only applicable phrase is “Look Out Below”.

So, the proper response is this:

instead of walking along and staring at the stars, keep a close eye on the

terrain directly in front of you. And

watch out for cliffs.

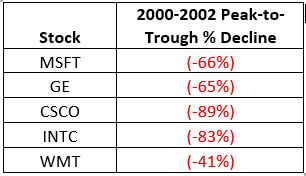

Top 5 companies as a % of S&P 500

Index

At times through history certain

stocks or groups of stocks catch “lightning in a bottle.” And when they do the advances are

spectacular, enriching anyone who gets on board – unless they happen to get on

board too late. Figure 3 displays the

percentage of the S&P 500 Index market capitalization made up by JUST the 5

largest cap companies in the index at any given point in time.

Figure 3 – Top 5 stocks as a % of

S&P 500 Index market cap (Courtesy: www.Bloomberg.com)

The anecdotal suggestion is pretty obvious. Following the market peak in 2000, the five stocks listed each took a pretty significant whack as shown in Figure 4.

Figure 4 – Top Stocks after the 2000 Peak

Then when we look at how far the line in Figure 3 has soared in 2020 the obvious inference is that the 5 stocks listed for 2020 are due to take a similar hit. And here is where it gets interesting. Are MSFT, AAPL, AMZN, GOOGL and FB due to lose a significant portion of their value in the years directly ahead?

Two thoughts:

*There is no way to know for sure

until it happens

*That being said, my own personal option

is “yes, of course they are”

But here is where the rubber meets

the road: Am I presently playing the bearish side of these stocks? Nope.

The trend is still bullish. Conversely,

am I keeping a close eye and am I willing to play the bearish side of these

stocks? Yup. But not until they – and the overall market –

actually starts showing some actual cracks.

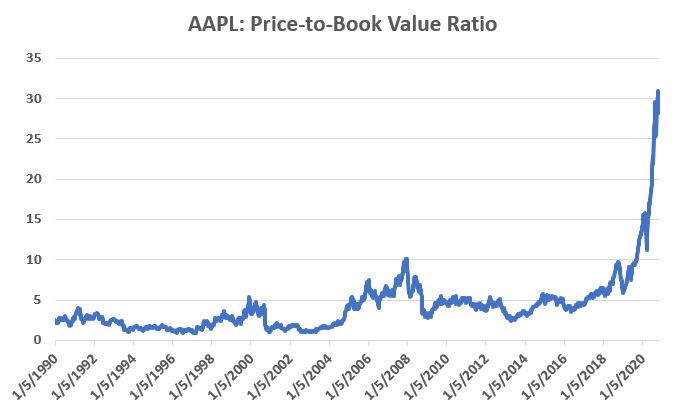

One Perspective on AAPL

Apple has been a dominant company for

many years, since its inception really.

Will it continue to be? I

certainly would not bet against the ability of the company to innovate and grow

its earnings and sales in the years ahead. Still timing – as they say – is everything. For what it is worth, Figure 5 displays the

price-to-book value ratio for AAPL since January 1990.

Figure 5 – AAPL price-to-book value ratio (Data courtesy of Sentimentrader.com)

Anything jump out at you?

Now one can argue pretty compellingly that price-to-book value is not the way to value a leading technology company. And I probably agree – to a point. But I can’t help but look at Figure 5 and wonder if that point has possibly been exceeded.

Summary

Nothing in this piece is meant to

make you “bearish” or feel compelled to sell stocks. For the record, I am still in the bullish

camp. But while this information DOES

NOT constitute a “call to action”, IT DOES constitute a “call to pay close

attention.”

Bottom line: enjoy the bull market

but DO NOT fall in love with it.

See also Jay Kaeppel Interview in July 2020 issue of Technical Analysis of Stocks and Commodities magazine

Disclaimer: The information, opinions and ideas expressed herein are for

informational and educational purposes only and are based on research conducted

and presented solely by the author. The

information presented represents the views of the author only and does not

constitute a complete description of any investment service. In addition, nothing presented herein should

be construed as investment advice, as an advertisement or offering of

investment advisory services, or as an offer to sell or a solicitation to buy

any security. The data presented herein

were obtained from various third-party sources.

While the data is believed to be reliable, no representation is made as

to, and no responsibility, warranty or liability is accepted for the accuracy

or completeness of such information.

International investments are subject to additional risks such as

currency fluctuations, political instability and the potential for illiquid

markets. Past performance is no

guarantee of future results. There is

risk of loss in all trading. Back tested

performance does not represent actual performance and should not be interpreted

as an indication of such performance.

Also, back tested performance results have certain inherent limitations

and differs from actual performance because it is achieved with the benefit of

hindsight.

Good news! Silver is above its price level of a year ago AND it is December! OK, maybe that is a bit too succinct. Perhaps a little more detail is in order.

Silver had a pretty terrific run from the March 2020 low to the July 2020 high, with silver futures rallying from 11.26 to 29.92 (to put it in more stark terms, the $ value of a silver futures contract increased from $56,300 to $149,600). But in recent weeks the “less shiny” metal has experienced enough of a pullback that a lot of traders are starting to turn away and refocusing on the soaring stock market.

While I claim no ability to “predict” the future price of silver, I have noticed that a couple of trends are presently suggesting that right now may be a good time NOT to give up on the stuff.

Two Factors Combined

For our purposes we will combine two

factors:

*Factor #1: The change in the

price of silver over the previous year

*Factor #2: The current month

of the year

From this we can create “Jay’s Silver

Model” (such as it is) as follows:

*If silver is above its price of 252

trading days ago then add +1 to the Model

*If the current month is January,

February, July, August, November or December then add +1 to the model

And there you have it. For any given trading day, the Model will

read 0, +1 or +2.

From here we will accumulate the

daily $ +(-) for a silver futures contract (each $1 movement in the price of a

silver futures contract is worth $5,000) based on the daily reading for Jay’s

Silver Model. The first date of the test

is July 20, 1971.

Does this matter? Well consider the following:

When Model = +2: Cumulative silver $ +(-) = +$273,205

When Model = +1: Cumulative silver $ +(-) = (-$57,700)

When Model = 0: Cumulative silver $ +(-) = (-$110,095)

In other words:

*While the Model read +2, silver gained

+$273,205

*While the Model was less than +2,

silver lost (-$167,865)

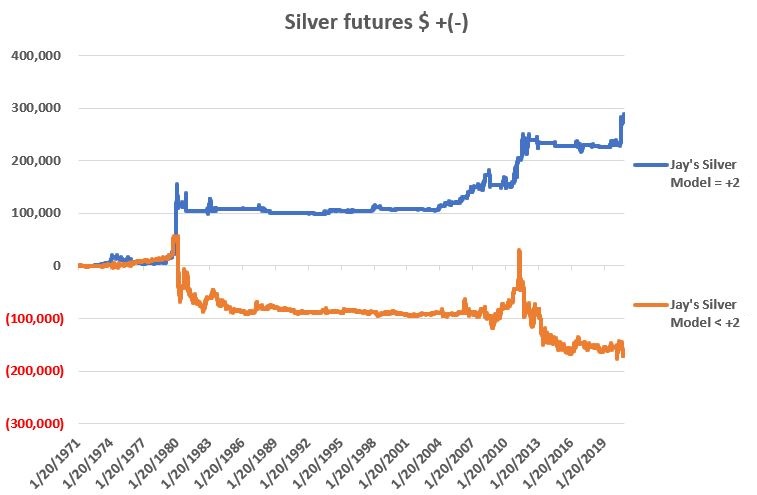

Figure 1 displays the cumulative

results.

Figure 1 – Cumulative $ +(-) for

silver futures is Jay’s Silver Model = +2 (blue) or Jay’s Silver Model < 2

(red); 1971-2020

The bad new “things” to note from

Figure 1 are:

*Silver can spend A LOT of time going

nowhere – even if the Model = +2

*There can ALWAYS be countertrend bullish

moves – even if the Model < +2

Still, the stark difference between

the two lines suggests that there might be some useful information – at the

very least on a “wight of the evidence” basis – conveyed for anyone looking to

trade silver.

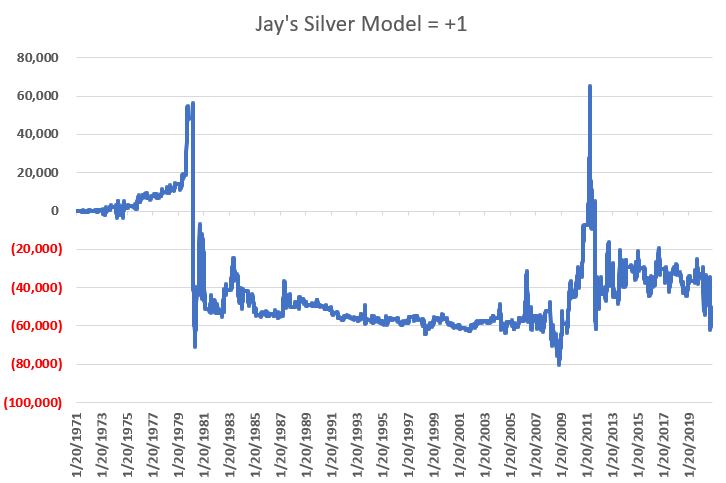

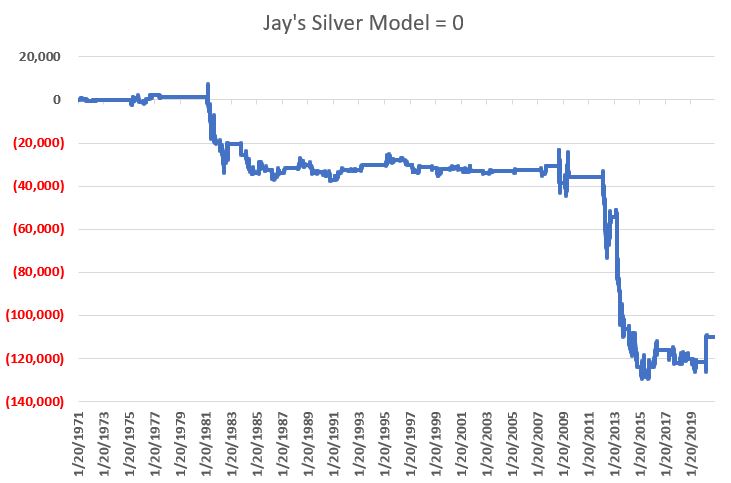

One other “interesting note” appears in Figures 2 and 3. Figure 2 displays the cumulative results for silver futures when the Model reads +1 and Figure 3 when the Model reads 0.

Figure 2 – Cumulative $ +(-) for

silver futures is Jay’s Silver Model = +1; 1971-2020

Figure 3 – Cumulative $ +(-) for

silver futures is Jay’s Silver Model = 0; 1971-2020

Note in Figure 2 that there were several massive countertrend rallies in silver while the Model read +1. However, in Figure 3 we see that very little good ever happens for silver when the Model reads 0.

To reiterate, Figure 3 displays the $ gain/loss from holding a long position in silver futures when:

A) silver is below its price level of 1 year ago (for the record I use 252 trading days with a 1-day lag) AND

B) The current month is NOT Jan., Feb., Jul., Aug., Nov. or Dec

Figure 4 displays the cumulative

(hypothetical) gain generated by:

*Holding a long position in silver

futures when the Model = +2

*Holding a flat position in silver

futures when the Model = +1

*Holding a short position in silver

futures when the Model = 0

Also displayed is the cumulative gain

from buying and holding a silver futures contract.

Figure 4 – Cumulative $ +(-) for

silver futures holding a long position if Jay’s Silver Model = +2 and a short

position if Jay’s Silver Model = 0; 1971-2020

The Current State of Affairs

*Silver is well above its price of one year ago (and that will remain the case as long as silver holds above roughly $18). So, Part 1 of the Model is positive.

*In addition, the second part of the model will remain bullish through the end of February 2021.

The bottom line is that the Model is pretty much “stuck on +2” for another 3 months. Does this “guarantee” that silver is certain to rise in the months ahead? Not at all. The Model was bullish all of November and during that time silver peaked and declined by 15% from that peak. So, there is nothing “magical” going on just because this silly little “Model” reads +2.

But history suggests that if you are going to play silver, it might be most prudent to play it from the long side, particularly as long as the recent support level of $21.81 (see Figure 5) holds.

Disclaimer: The information, opinions and ideas expressed herein are for

informational and educational purposes only and are based on research conducted

and presented solely by the author. The

information presented represents the views of the author only and does not constitute

a complete description of any investment service. In addition, nothing presented herein should

be construed as investment advice, as an advertisement or offering of

investment advisory services, or as an offer to sell or a solicitation to buy

any security. The data presented herein

were obtained from various third-party sources.

While the data is believed to be reliable, no representation is made as

to, and no responsibility, warranty or liability is accepted for the accuracy

or completeness of such information.

International investments are subject to additional risks such as

currency fluctuations, political instability and the potential for illiquid

markets. Past performance is no

guarantee of future results. There is

risk of loss in all trading. Back tested

performance does not represent actual performance and should not be interpreted

as an indication of such performance.

Also, back tested performance results have certain inherent limitations

and differs from actual performance because it is achieved with the benefit of

hindsight.

It is not exactly a little-known fact

that the performance of small-cap stocks relative to large-cap stocks

experiences something of an ebb and flow.

It is also not exactly a secret that December into February has tended

to see the market favor small-caps. I

will explain why this is as soon as I come up with something plausible. Kidding.

As a proud graduate of “The School of Whatever Works” I tend to spend

less time focusing on “Why” and more time focusing on “When.”

The Small-Cap Sweet Spot

Our supposed “favorable period” for

small-caps extends:

*From the close on December Trading Day #11 (12/15/20 this year) through the close of February Trading Day #11 (2/16/2021)

The Test

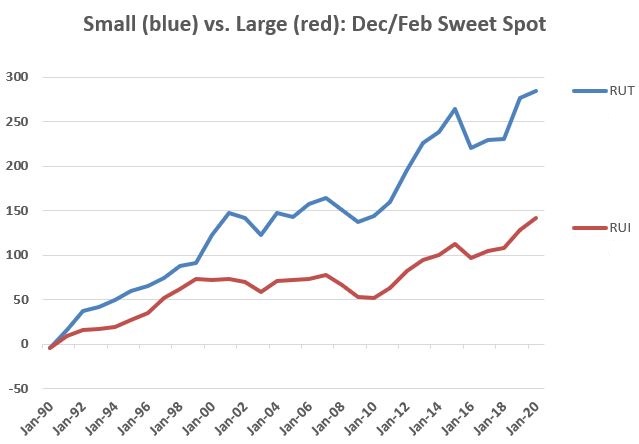

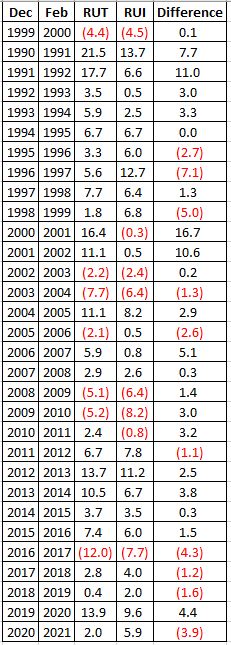

How has this worked out in the past? To test results, we will use the Russell 2000 (RUT) to measure small-cap performance and the Russell 1000 (RUI) to measure large-cap performance. Note that all results use price data only, NOT total return.

Figure 1 displays the cumulative %

growth for both small-cap and large-cap ONLY during the Small-Cap Sweet Spot

Now if I were smart, I would state something

like “so clearly small-caps outperform large-caps during mid-Dec through

mid-Feb!” and “The End.”

Unfortunately, I am not that smart.

Because the reality is that there is nothing “certain” about this relationship and as it turns out, even during a seemingly favorable for small-caps period there is still an “ebb and flow”. First some numbers.

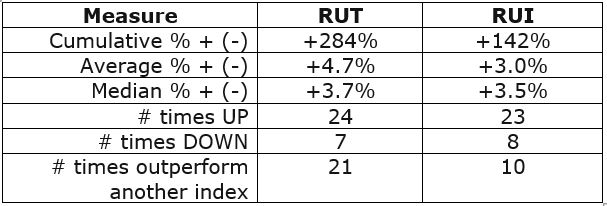

Figure 2 – Facts and Figures

Clearly small-caps have tended to

outperform large caps during mid-Dec through mid-Feb. But there are a few caveats to keep in mind:

#1. There can and will be losing periods

RUT has lost money mid-Dec to mid-Feb

in 7 of the last 31 years. While a 77%-win

rate is outstanding in the financial markets, it also means that loses occurred

23% of the time. No one gets into

small-caps in mid-December and gets out with a loss two months later and says, “Well,

at least there is still a 77%-win rate!”

They get out and say “Well that sucked” and shake their head wondering “what

did I think that was a good idea?”

Which lends itself nicely to invoking….

Jay’s Trading Maxim #27: In the financial markets, the difference between theory

and reality can occasionally be a chasm a mile wide.

#2. Losses can be relatively large

In 2003-2004 RUT lost -7.7% during

the Sweet Spot and in 2016-2017 the loss was -12.0%. So, there’s that (you have officially been

warned).

One piece of positive news, when it

comes to double-digit gains and losses:

*# times RUT Sweet Spot gain > 10%

= 8

*# times RUT Sweet Spot loss < -10% = 1

#3. RUT has underperformed RUI in four of the last five “Sweet Spots”

As I said, there is no “sure thing” here. For the record, there is a part of me that suspects that since things have “ebbed” in 4 of the last 5 years (i.e., small underperforming large), that a return to “flow” (i.e., small-caps outperforming) may be in the cards. Unfortunately, only time will tell.

Summary

Small-cap stocks have demonstrated a

historical seasonal tendency to, a) advance in price, and, b) outperform large

caps during the Seasonal Sweet Spot detailed above.

Whether or not it is worth attempting

to exploit via an actual trade is left to the reader.

Figure 3 – Year-by-year results

See also Jay Kaeppel Interview in July 2020 issue of Technical Analysis of Stocks and Commodities magazine

Disclaimer: The information, opinions and ideas expressed herein are for

informational and educational purposes only and are based on research conducted

and presented solely by the author. The

information presented represents the views of the author only and does not

constitute a complete description of any investment service. In addition, nothing presented herein should

be construed as investment advice, as an advertisement or offering of

investment advisory services, or as an offer to sell or a solicitation to buy

any security. The data presented herein

were obtained from various third-party sources.

While the data is believed to be reliable, no representation is made as

to, and no responsibility, warranty or liability is accepted for the accuracy

or completeness of such information.

International investments are subject to additional risks such as

currency fluctuations, political instability and the potential for illiquid

markets. Past performance is no

guarantee of future results. There is

risk of loss in all trading. Back tested

performance does not represent actual performance and should not be interpreted

as an indication of such performance.

Also, back tested performance results have certain inherent limitations

and differs from actual performance because it is achieved with the benefit of

hindsight.

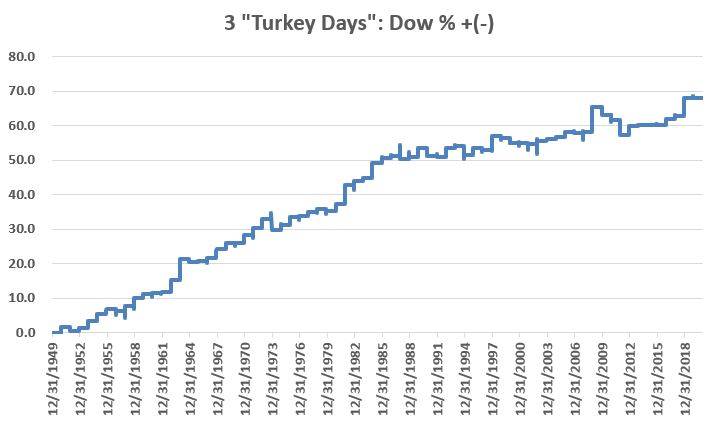

The trading days around holidays have a long-term tendency to be bullish for the stock market. While I typically stick to the “3 trading days before and 3 trading days after” a holiday as “the bullish period”, with Thanksgiving it might make sense to cut things a little finer.

The Big 3 Turkey Days

The best time around Thanksgiving has

tended to be the two trading days before (Tuesday and Wednesday) and the day

after (Friday). The good news is that period

has been consistently bullish over time.

The “bad news” is that it appears to have been slightly less effective in

recent years.

For our purposes we will measure the price

change for the Dow Jones Industrial Average from the close on Monday the week

of Thanksgiving and the close on Friday of the same week.

Figure 1 displays the cumulative %

growth.

Figure 1 – Cumulative Dow % +(-) 2

days before and 1 day after Thanksgiving; 1950-2019

The cumulative growth from 1950

through 2019 was +68.0%. If that doesn’t

seem like much just remember that we are talking about just 3 trading days a

year.

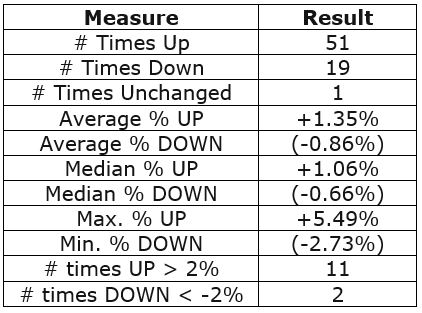

Figure 2 displays some of the relevant facts and figures

Figure 2 – Relevant Facts and Figures

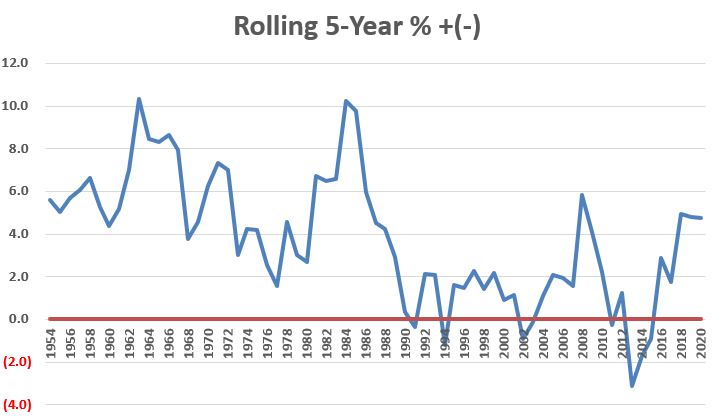

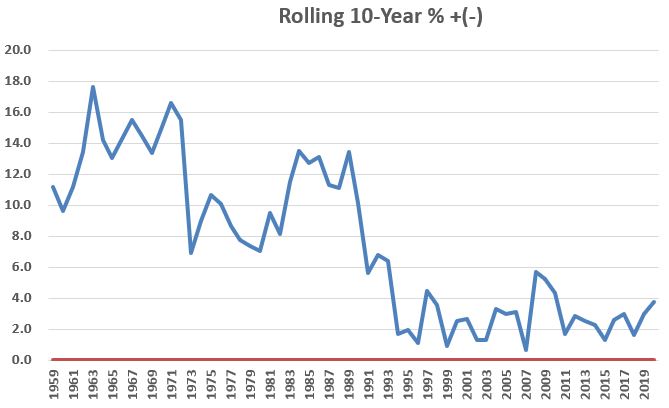

Figure 3 displays the rolling 5-year

return and Figure 4 displays the rolling 10-year return. For what it is worth,

returns have come down in recent years.

This may be due to more people being aware of these types of seasonal

trends (thanks to blabbermouths like yours truly?).

Figure 3 – Rolling 5-year returns

Figure 4 – Rolling 10-year returns

Figure 5 below displays the year-by-year 3-day results for the Dow.

Year

3 “Turkey” Day Dow % +(-)

1950

1.7

1951

(1.1)

1952

0.9

1953

1.7

1954

2.2

1955

1.2

1956

(0.4)

1957

1.2

1958

2.3

1959

0.9

1960

0.3

1961

0.3

1962

3.0

1963

5.5

1964

(0.8)

1965

0.2

1966

0.6

1967

2.3

1968

1.4

1969

(0.1)

1970

1.8

1971

1.7

1972

2.0

1973

(2.4)

1974

1.1

1975

1.8

1976

0.1

1977

1.0

1978

0.6

1979

(0.4)

1980

1.5

1981

4.0

1982

0.7

1983

0.7

1984

3.0

1985

1.1

1986

0.4

1987

(0.7)

1988

0.4

1989

1.7

1990

(1.5)

1991

(0.3)

1992

1.8

1993

0.4

1994

(1.6)

1995

1.3

1996

(0.4)

1997

2.6

1998

(0.4)

1999

(0.9)

2000

0.1

2001

(0.2)

2002

0.5

2003

0.4

2004

0.3

2005

1.0

2006

(0.3)

2007

0.2

2008

4.6

2009

(1.3)

2010

(0.8)

2011

(2.7)

2012

1.7

2013

0.1

2014

0.1

2015

0.0

2016

1.0

2017

0.5

2018

3.2

2019

(0.1)

2020

?

Figure 5 – Year-by-year results

Happy Thanksgiving!

See also Jay Kaeppel Interview in July 2020 issue of Technical Analysis of Stocks and Commodities magazine

Disclaimer: The information, opinions and ideas expressed herein are for

informational and educational purposes only and are based on research conducted

and presented solely by the author. The

information presented represents the views of the author only and does not constitute

a complete description of any investment service. In addition, nothing presented herein should

be construed as investment advice, as an advertisement or offering of

investment advisory services, or as an offer to sell or a solicitation to buy

any security. The data presented herein

were obtained from various third-party sources.

While the data is believed to be reliable, no representation is made as

to, and no responsibility, warranty or liability is accepted for the accuracy

or completeness of such information.

International investments are subject to additional risks such as

currency fluctuations, political instability and the potential for illiquid

markets. Past performance is no

guarantee of future results. There is

risk of loss in all trading. Back tested

performance does not represent actual performance and should not be interpreted

as an indication of such performance.

Also, back tested performance results have certain inherent limitations

and differs from actual performance because it is achieved with the benefit of

hindsight.

The U.S. Dollar has been in a pretty

prolonged slump since spiking to a top in March of this year. Any chance for a rebound? Sure, there is always a chance. The buck is pretty oversold and trader

sentiment – a typically contrarian indicator – is pretty darn negative. So, a “bounce” would not be entirely

unexpected.

Still, the view from where I sit is

that the dollar is in the midst of a longer-term decline.

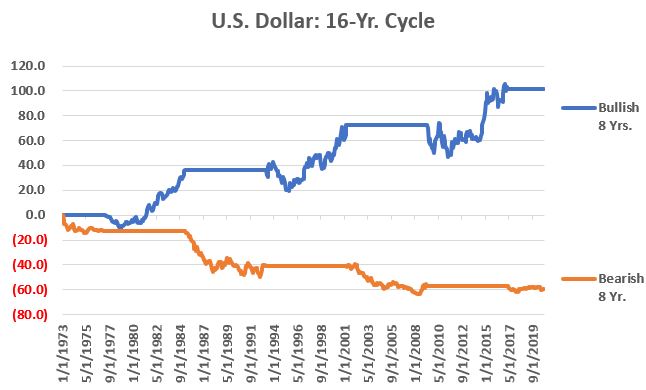

The Long-Term Cycle

I read a number of years ago about a

16-year cycle for the U.S. dollar.

Unfortunately, I can’t remember where I read it so I cannot give proper

credit. I have read about this cycle

again recently. For the record, it seems

to follow the cycle with a slightly different start/end date than some sources

I have seen recently. No matter. We are not talking about “precision market

timing” here, just a basic overarching trend.

So, let’s take a closer look.

The U.S. Dollar 16-Year Cycle

The first full 16-year cycle – by my account – began on 3/31/1969 (NOTE: the first date of data I have available is 1/31/1973 – so results below start in 1973). The “bearish” phase ran from then through 3/31/1977 and the “bullish” phase ran from 3/31/1977 through 3/31/1985. And so on and so forth. Figure 1 displays the cumulative % growth achieved by holding a hypothetical long position in the U.S. dollar during all bullish phases (blue line) and bearish phases (orange line).

Figure 1 – Cumulative % +(-) for U.S.

dollar during Bullish 8 year phases (blue) and Bearish 8 year phases (orange)

Figure 2 displays the results by the numbers.

Figure 2 – U.S. Dollar during bull and bear phases of 16-year cycle (NOTE: 1st Bearish Phase began 3/31/1969, HOWOEVER, the 1st day of available data is 1/31/1973)

The latest phase – a bearish phase –

began on 3/31/2017 and extends through 3/31/2025. Does that mean the dollar is doomed to

decline relentlessly for another 4+ years?

Not at all. It does tell us

however, that it may be wise to favor the bearish side on any trade involving

the U.S. dollar.

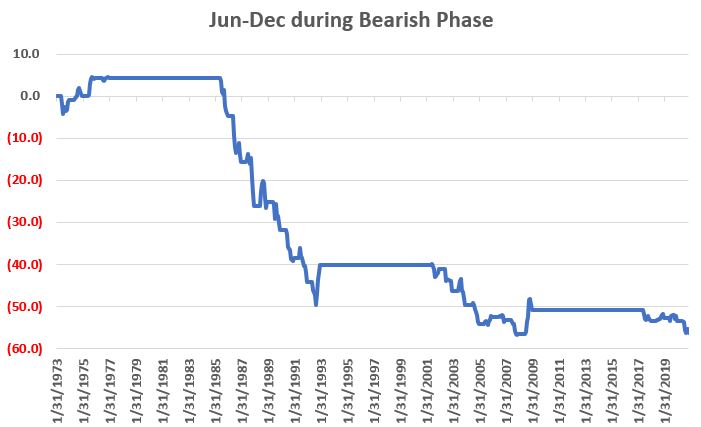

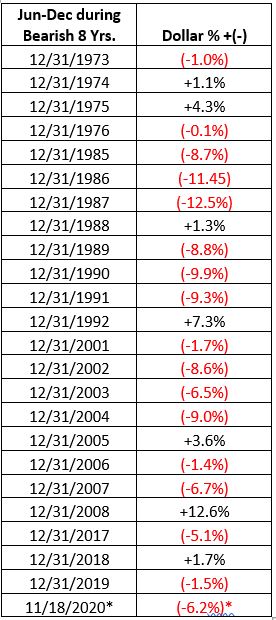

Digging a Little Deeper

Historically the most challenging

time for the dollar is:

*During the months of June through

December when the 16-year cycle is in a bearish phase

Figure 3 displays the cumulative %

growth achieved by holding a hypothetical long position in the U.S. dollar ONLY

during the months of June through December during those years when the 16-year

cycle is bearish (the most recent such period began on June 1st of

this year and extends through December 31st).

Figure 3 – U.S. Dollar cumulative %

+(-) during June through December within bearish 8-year phase

Figure 4 displays the year-by-year

results (i.e., the % gain/loss for the dollar during June through December ONLY

during those years when the 16-year cycle is bearish).

Figure 4 – U.S. Dollar % +(-) during

June through December within bearish 8-year phase

*- thru 11/18/20

Summary

There is absolutely nothing that

requires the U.S. dollar to adhere to the 16-year cycle detailed above. But history suggests that getting bearish during

the bullish 8-year phase and/or getting bullish during the bearish 8-year phase

typically involves being willing to “swim upstream.”

A large part of any investment

success is “identifying the flow” and “going with said flow.” The dollar will remain in a bearish phase

through March 2025. Therefore, history

suggests that June-Dec of 2021, 2022, 2023 and 2024 may be a time to consider a

bearish position re the buck.

See also Jay Kaeppel Interview in July 2020 issue of Technical Analysis of Stocks and Commodities magazine

Disclaimer: The information, opinions and ideas expressed herein are for

informational and educational purposes only and are based on research conducted

and presented solely by the author. The

information presented represents the views of the author only and does not

constitute a complete description of any investment service. In addition, nothing presented herein should

be construed as investment advice, as an advertisement or offering of investment

advisory services, or as an offer to sell or a solicitation to buy any

security. The data presented herein were

obtained from various third-party sources.

While the data is believed to be reliable, no representation is made as

to, and no responsibility, warranty or liability is accepted for the accuracy

or completeness of such information.

International investments are subject to additional risks such as

currency fluctuations, political instability and the potential for illiquid

markets. Past performance is no

guarantee of future results. There is

risk of loss in all trading. Back tested

performance does not represent actual performance and should not be interpreted

as an indication of such performance.

Also, back tested performance results have certain inherent limitations

and differs from actual performance because it is achieved with the benefit of

hindsight.

*”Every situation in life represents an opportunity”

*”Opportunity is where you find it”

Nowhere is this truer than in the

financial markets.

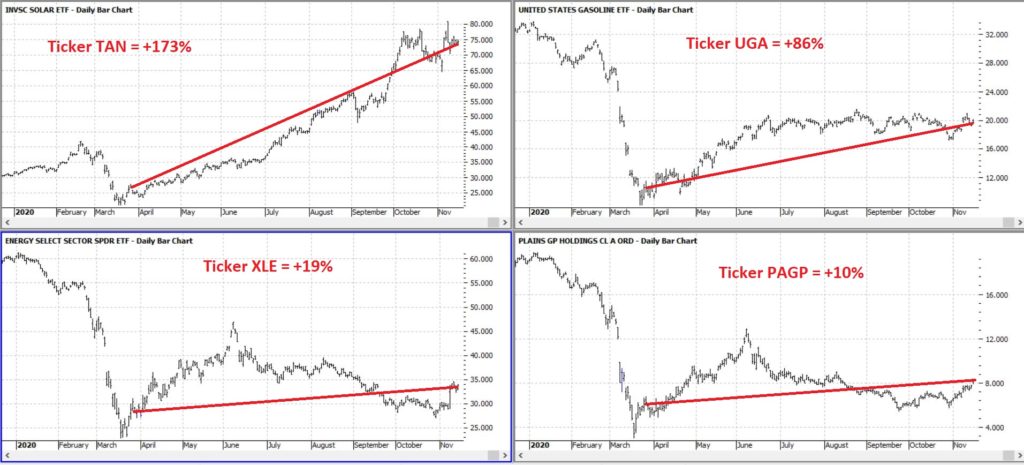

To wit, in this article dated 3/26/2020 (cue the scary music) – when things looked their absolute worst – I highlighted four tickers in the energy sector (yes, THAT energy sector, the one that has been a disaster and loathed and unloved for some time now). Now it would have taken a true “Buy when there is blood in the streets” mentality, and/or almost foolhardy nerves of steel to actually pile into those issues at the time.

But that is sort of the point.

Figure 1 displays the tickers and their price action since the close on 3/26/2020.

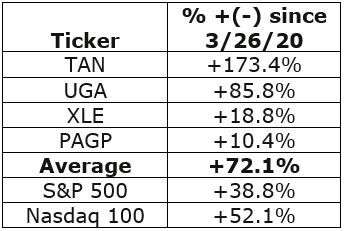

Figure 2 displays the comparative

performance versus the S&P 500 and the Nasdaq 100.

Figure 2 – “Blood in the Streets” energy stocks versus major indexes

As you can see in Figure 2 these four

stocks as a whole have actually outperformed both the S&P 500 Index and the

Nasdaq 100 Index.

Now the point IS NOT that I am some

great stock-picker (because I am not).

The point is that, well, see the two quotes above.

A Broader Look at Energy

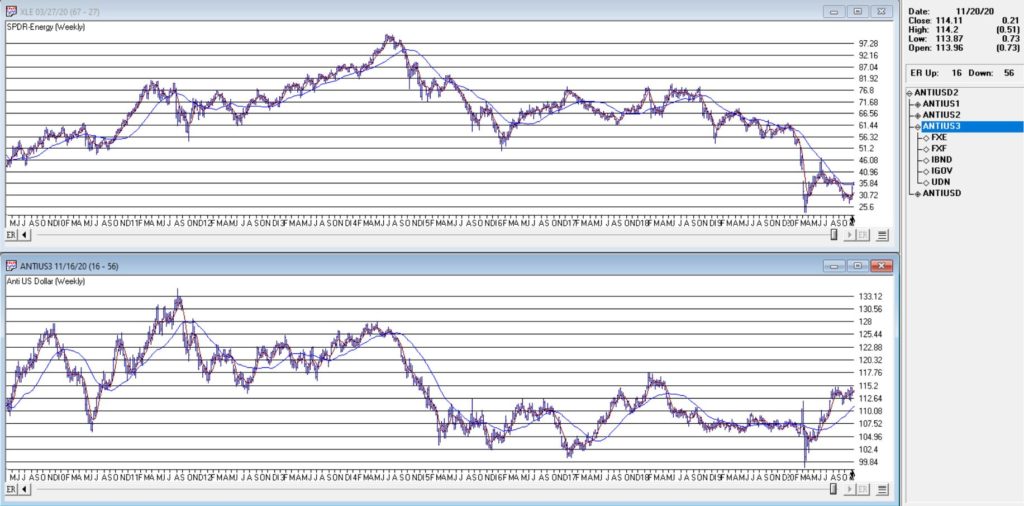

For someone with less of the “buy when there is blood in the streets” mentality and more of “trend-following” mentality, a simple trend-following method may soon (at long last) swing to the bullish side.

It works like this:

*Two “tickers” see their respective

5-week average cross above their respective 30-week average

*Ticker 1 is ticker XLE (the SPDR

energy ETF)

*Ticker 2 is an index (I created) of

securities that have an inverse correlation to the U.S. Dollar

You can see these two – along with

their respective 5-week and 30-week – in Figure 3.

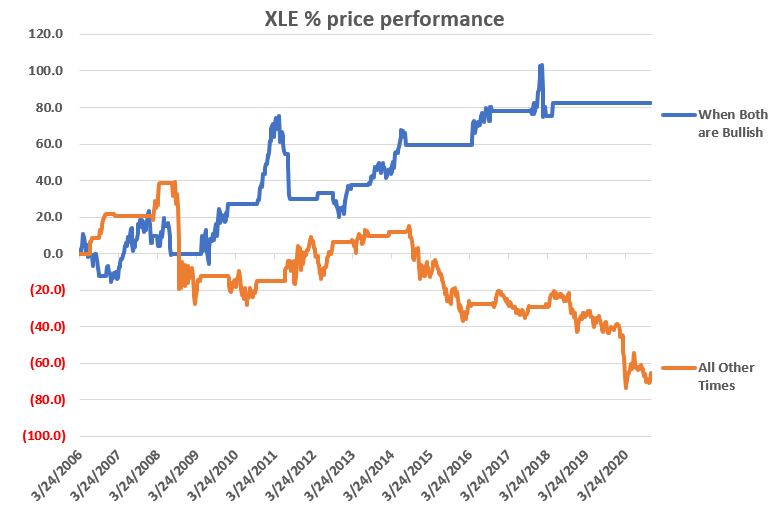

As you can see in Figure 3 the two have a tendency to often move together. At other times they do not. The key point here is that we ONLY pay attention when the two tickers are both trending in the same direction.

Why is this important?

Figure 4 displays the cumulative

price growth for ticker XLE (as a proxy for the broad energy sector) under two separate

circumstance:

*When BOTH XLE and ANTIUS3 are in

uptrends (i.e., 5-week average ABOVE 30-week average)

*When EITHER XLE or ANTIUS3 is NOT in

an uptrend (i.e., 5-week average BELOW 30-week average)

Figure 4 – XLE cumulative %+(-) depending

on trend status for XLE and ANTIUS3

To put it in numbers:

When BOTH are in Uptrends: XLE = +82.3%

When EITHER is NOT in an Uptrend: XLE

= -65.5%

Summary

Another glance at Figure 1 reveals

that ANTIUS3 is in an uptrend and that XLE is not quite there yet. So, at the moment there is no bullish signal

from the method described above. However,

energy does appear to be “trying” to rally.

Investors looking for “opportunity” may be wise to keep an eye on the 5-week

and 30-week averages of ticker XLE in the weeks and month ahead.

See also Jay Kaeppel Interview in July 2020 issue of Technical Analysis of Stocks and Commodities magazine

Disclaimer: The information, opinions and ideas expressed herein are for

informational and educational purposes only and are based on research conducted

and presented solely by the author. The

information presented represents the views of the author only and does not

constitute a complete description of any investment service. In addition, nothing presented herein should

be construed as investment advice, as an advertisement or offering of

investment advisory services, or as an offer to sell or a solicitation to buy

any security. The data presented herein

were obtained from various third-party sources.

While the data is believed to be reliable, no representation is made as

to, and no responsibility, warranty or liability is accepted for the accuracy

or completeness of such information.

International investments are subject to additional risks such as

currency fluctuations, political instability and the potential for illiquid

markets. Past performance is no

guarantee of future results. There is

risk of loss in all trading. Back tested

performance does not represent actual performance and should not be interpreted

as an indication of such performance.

Also, back tested performance results have certain inherent limitations

and differs from actual performance because it is achieved with the benefit of

hindsight.